Uninsured Driver Claims Explained: Your 2026 Guide

An uninsured driver claim is a first-party insurance claim you file against your own policy when the at-fault driver carries no liability insurance or not enough to cover your losses. The industry standard term is an uninsured motorist (UM) or underinsured motorist (UIM) claim, and understanding the difference matters from the moment you leave the accident scene. This coverage acts as a financial safety net that replaces what the at-fault driver’s insurer would have paid. Without it, your only option is suing an individual who likely has no assets worth pursuing. Knowing what is uninsured driver claim coverage, how it works, and what traps to avoid can be the difference between full recovery and paying your own medical bills.

What qualifies as an uninsured or underinsured driver?

The distinction between uninsured and underinsured drivers is more than a technicality. It determines which part of your policy applies and how your claim gets processed.

Uninsured drivers are motorists who carry zero liability insurance at the time of the accident. This is more common than most people realize. Many drivers let their policies lapse after a premium increase, and you have no way of knowing until after the crash.

Underinsured drivers carry liability insurance, but their policy limits fall short of your actual damages. For example, if a driver carries $25,000 in bodily injury liability but your medical bills reach $80,000, the gap of $55,000 is where your UIM coverage steps in.

Hit-and-run accidents also fall under the uninsured motorist umbrella. If a driver flees the scene and cannot be identified, your UM coverage treats the situation as if the at-fault driver had no insurance. Many states require physical contact between vehicles before a hit-and-run qualifies, meaning a “phantom vehicle” that forces you off the road without touching your car may not trigger coverage in those states.

Here is a quick breakdown of the qualifying scenarios:

- No insurance at all: Driver has zero active liability coverage at the time of the crash.

- Lapsed policy: Driver had insurance but missed payments, voiding the policy before the accident.

- Insufficient limits: Driver’s liability limits are too low to cover your full damages, triggering UIM coverage.

- Hit-and-run: At-fault driver flees and cannot be identified; physical contact rules vary by state.

- Phantom vehicle: An unidentified vehicle causes the crash without making contact; coverage depends on your state’s rules.

- Stolen vehicle: Some states exclude coverage when the at-fault vehicle was stolen; check your policy terms.

Understanding which category applies to your situation shapes every step of the claim process for uninsured drivers from the first phone call to your insurer.

How do uninsured motorist claims work?

Uninsured motorist coverage splits into two distinct components, and knowing both protects you from gaps in recovery.

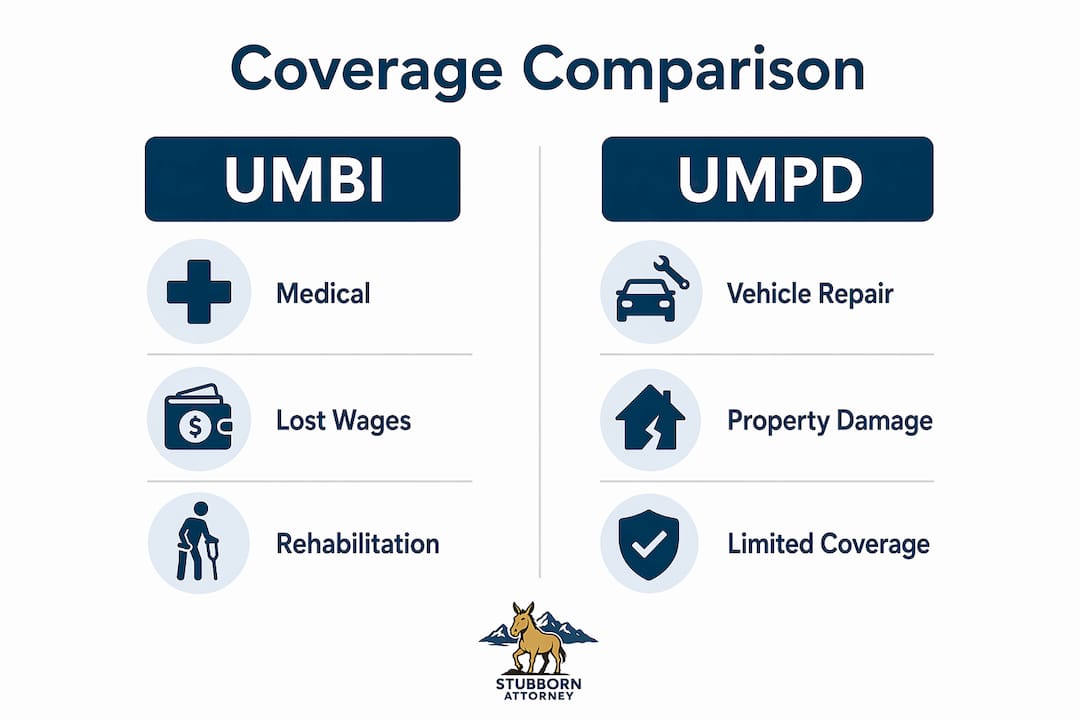

UMBI vs. UMPD: what each covers

UMBI (Uninsured Motorist Bodily Injury) covers medical bills, lost wages, rehabilitation costs, and pain and suffering when an uninsured driver causes the accident. It does not cover vehicle damage. That is a critical point many accident victims miss: your bodily injury claim and your property damage claim run on separate tracks.

UMPD (Uninsured Motorist Property Damage) covers your vehicle repairs when an uninsured driver is at fault. UMPD coverage varies by state, often carries a deductible, and is not available everywhere. Drivers in states without UMPD typically rely on their collision coverage to repair their vehicle, which means paying their collision deductible even though they did nothing wrong.

The step-by-step claim filing process

Filing a UM or UIM claim follows a structured sequence. Skipping steps or getting the order wrong can cost you coverage.

- Call the police immediately. A police report documents the at-fault driver’s lack of insurance and establishes the facts of the accident. Without it, your insurer has grounds to question your account.

- Notify your insurer promptly. Report the accident to your own insurance company as soon as possible. Delays beyond 24–48 hours can be treated as “prejudice” by your insurer, giving them a legal basis to deny your claim.

- Gather evidence at the scene. Photograph all vehicle damage, road conditions, traffic signals, and any visible injuries. Collect contact information from witnesses before they leave.

- Seek medical attention immediately. Even if you feel fine, get evaluated. Delayed injury symptoms are common after crashes, and a gap in medical care gives adjusters a reason to argue your injuries were not caused by the accident.

- Request the at-fault driver’s insurance information. If they have none, document that fact. A DMV records check or police report notation confirming no active policy is the evidence your insurer needs.

- Submit your medical records and bills. Your insurer will request documentation of every expense. Organize records chronologically and keep copies of everything you send.

- Follow up in writing. Every conversation with your insurer should be confirmed in an email or letter. Written records protect you if the insurer later disputes what was discussed.

Pro Tip: Before you give your insurer a recorded statement, consult an attorney. Insurance adjusters use recorded statements to find inconsistencies that justify denying or reducing your claim. You have the right to speak with legal counsel first.

Your policy’s limits cap what you can recover. If your UMBI limit is $100,000 and your damages total $150,000, you absorb the $50,000 difference unless you have additional coverage. Review your types of insurance coverage before an accident happens, not after.

What are the common challenges in uninsured driver claims?

The most important thing to understand about a UM or UIM claim is this: your own insurance company is not on your side. Your insurer becomes the opposing party in the dispute, and their financial interest is to pay you as little as possible. That conflict of interest shapes every tactic they use.

“In a UM/UIM claim, you are essentially suing your own insurance company. They have a team of adjusters and lawyers whose job is to minimize your payout. You need someone in your corner who knows how they operate and refuses to back down.”

Common challenges accident victims face include:

- Proving the driver was uninsured. Your insurer will not simply take your word for it. You need a police report, a DMV records check, or written confirmation from the at-fault driver’s alleged insurer that no valid policy existed at the time of the crash.

- Recorded statement traps. Adjusters often request a recorded statement within days of the accident, before you fully understand your injuries or the claim’s value. Statements made early can be used to contradict later medical findings.

- Lowball settlement offers. Initial offers frequently undervalue future medical costs, long-term lost wages, and non-economic damages like pain and suffering. Accepting early locks you out of further recovery.

- Claim denial for late reporting. Failure to notify your insurer promptly can be legally construed as prejudice to the insurer, allowing them to deny your claim entirely. Report the accident the same day it happens.

- Arbitration clauses. Many UM policies require binding arbitration to resolve disputes over claim value. This means you cannot take the insurer to court if you disagree with their offer. The arbitration process has its own rules, timelines, and strategic considerations.

- Pre-existing injury disputes. Insurers routinely argue that your injuries existed before the accident. Thorough medical documentation from immediately after the crash is your best defense against this tactic.

Pro Tip: Hire a personal injury attorney before you accept any settlement offer. An attorney who knows how to strengthen injury claims after a car accident can identify damages you may have overlooked and negotiate from a position of knowledge.

The legal rights for uninsured claims are real, but they require active protection. Passivity in a UM claim almost always results in a lower recovery.

How do state laws affect uninsured motorist coverage?

State law determines whether you even have uninsured motorist coverage and how much protection it provides. The variation across states is significant enough to change your entire legal strategy.

As of 2026, 22 states and Washington D.C. mandate that drivers carry some form of UM or UIM bodily injury coverage. That means in the remaining states, insurers must offer the coverage, but drivers can reject it in writing. Many do, leaving themselves exposed.

The table below summarizes the key coverage variables that differ by state:

| Coverage Variable | Mandatory States | Optional States |

|---|---|---|

| UM bodily injury (UMBI) | Required by law | Offered; can be rejected in writing |

| UIM bodily injury | Often bundled with UM | May require separate election |

| UM property damage (UMPD) | Available in some states | Not offered in all states |

| UMPD deductible | Varies; often $200–$300 | Varies by policy |

| Stacking of limits | Permitted in some states | Prohibited in others |

| Physical contact rule (hit-and-run) | Required in many states | Not required in all states |

Stacking refers to combining UM limits across multiple vehicles on your policy. If you insure three cars with $50,000 UMBI each, stacking allows you to claim up to $150,000 on a single accident. Some states prohibit stacking entirely. Others allow it only if you pay an additional premium for the privilege.

Property damage deductibles also vary. As a reference point, the UK’s Motor Insurers’ Bureau applies a mandatory £300 deductible to property damage claims against uninsured drivers. American states handle this differently, with UMPD deductibles typically set by individual policy terms rather than a national standard.

Your state’s department of insurance website is the authoritative source for your specific requirements. Colorado drivers can also review Colorado-specific car accident claim options to understand how state law applies to their situation.

What I’ve learned after a decade of fighting these claims

After more than ten years handling personal injury cases in Colorado, and before that working as a claims adjudicator for the federal government, I have seen the same mistake repeat itself constantly. People treat their own insurance company as a partner after an uninsured driver accident. They answer every question, give recorded statements on day two, and accept the first settlement offer because they are exhausted and in pain. That is exactly what the insurer counts on.

The uncomfortable truth is that your insurer has a financial incentive to pay you less. The UM claim process is functionally a lawsuit against your own policy, and the company on the other side of that dispute has lawyers, adjusters, and years of experience minimizing payouts. You are dealing with this for the first time. That asymmetry is real, and it matters.

What actually works is treating the claim like the legal proceeding it is from day one. Document everything. Report immediately. Get medical care on record before symptoms worsen. And before you say anything substantive to an adjuster, talk to an attorney. Not because attorneys are necessary in every case, but because knowing your rights before you waive them is always the right move.

UM coverage is a genuine safety net, but it is not a guarantee of full recovery. The coverage limit, your state’s rules, and how well you document your claim all determine what you actually receive. I have seen clients with strong cases recover far less than they deserved because they handled the first two weeks alone. I have also seen clients with complicated claims recover fully because they protected their rights early. The difference is almost always preparation and persistence.

— Ryan

When an uninsured driver hits you: Stubbornattorney can help

Uninsured driver claims are legally complex, and the stakes are high. Stubbornattorney, the brand home of Malnar Injury Law, represents only injured victims across Colorado. Ryan Malnar spent years as a federal claims adjudicator before becoming a personal injury attorney, which means he knows exactly how insurers evaluate and undervalue claims. If you were hit by an uninsured or underinsured driver, reviewing common personal injury case examples is a useful first step to understanding where your situation fits. A free case evaluation costs you nothing and gives you a clear picture of what your claim is actually worth before you talk to any adjuster.

FAQ

What is an uninsured driver claim?

An uninsured driver claim is a first-party insurance claim you file against your own UM or UIM policy when the at-fault driver has no insurance or insufficient coverage to pay your damages. It covers medical bills, lost wages, and pain and suffering up to your policy’s limits.

Does uninsured motorist coverage pay for vehicle damage?

UMBI does not cover vehicle damage. You need separate UMPD coverage for that, and UMPD is not available in all states. Drivers without UMPD typically use their collision coverage to repair their vehicle after an uninsured driver accident.

How long do I have to file an uninsured motorist claim?

You must notify your insurer as soon as possible after the accident. Delays beyond 24–48 hours can be treated as prejudice by your insurer, which may result in a full claim denial. Formal filing deadlines vary by state and policy, so report immediately and confirm deadlines in writing.

Can my insurer deny an uninsured motorist claim?

Yes. Insurers can deny UM claims for late reporting, failure to prove the driver was uninsured, policy exclusions, or procedural violations. Consulting a personal injury attorney before responding to your insurer’s requests significantly reduces the risk of a wrongful denial.

Do all states require uninsured motorist coverage?

No. 22 states and Washington D.C. mandate some form of UM bodily injury coverage. In the remaining states, insurers must offer the coverage, but drivers can reject it in writing. Check your state’s department of insurance for the specific requirements that apply to your policy.