How to Estimate Damages After a Car Accident

Estimating damages is the process of quantifying both your actual financial losses and the intangible harms that result from a car accident. In legal terms, this falls under compensatory damages, which split into two categories: economic and non-economic. Knowing how to estimate damages accurately determines how much compensation you can realistically pursue through an insurance claim or a personal injury lawsuit. The methods are not guesswork. They follow recognized frameworks used by attorneys, insurance adjusters, and forensic economists every day. This guide walks you through each category, the calculation methods behind them, and the documentation habits that protect your claim from the start.

What are the types of damages to estimate after a car accident?

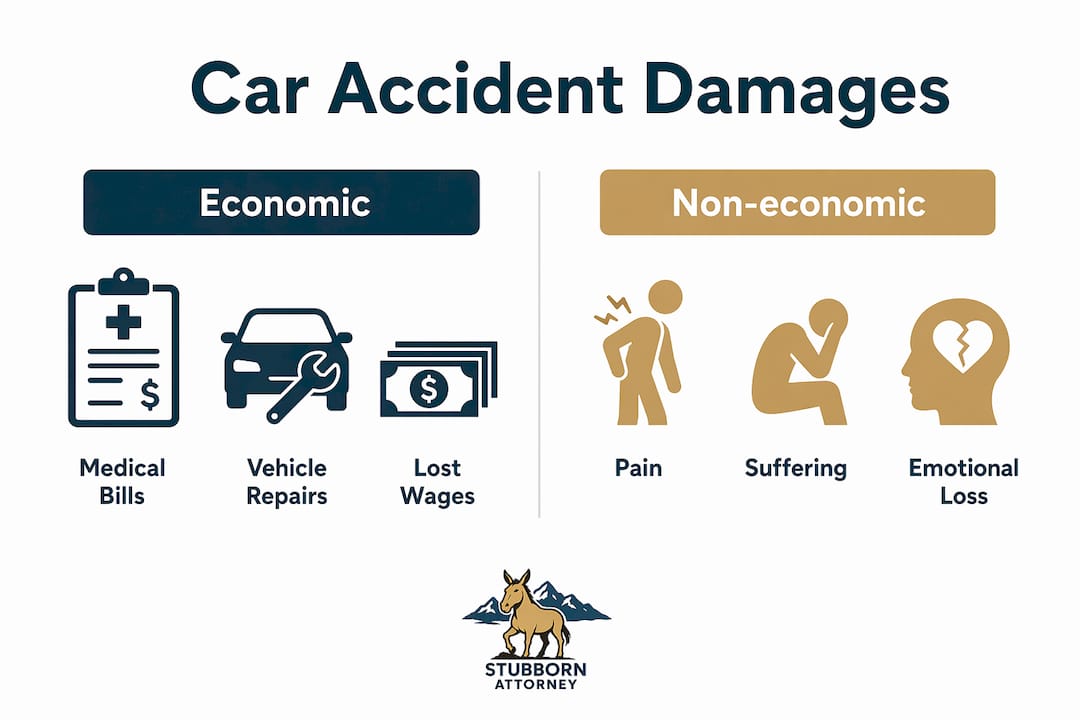

Compensatory damages cover every loss tied to the accident, and they divide cleanly into two groups. Understanding both groups before you start calculating prevents you from leaving money on the table.

Economic damages

Economic damages are your verifiable, dollar-for-dollar losses. They include:

- Medical expenses: Emergency room bills, surgery costs, physical therapy, prescription medications, and any future treatment your doctor projects as necessary.

- Lost wages: Income you missed while recovering, including sick days, vacation time you were forced to use, and reduced hours.

- Lost earning capacity: If your injuries permanently limit your ability to work at the same level, the difference in lifetime earnings counts as a damage.

- Property damage: The cost to repair or replace your vehicle and any personal property destroyed in the crash.

- Out-of-pocket costs: Transportation to medical appointments, home care assistance, and adaptive equipment.

Each of these losses has a paper trail. Receipts, pay stubs, tax returns, and repair estimates all serve as direct evidence. That documentation is what makes economic damages the foundation of any claim.

Non-economic damages

Non-economic damages compensate for losses that do not show up on a bill. These include pain and suffering, emotional distress, loss of enjoyment of life, and loss of consortium for a spouse or family member. They are real losses, but they require a different calculation method because no invoice exists for them.

Punitive damages

Punitive damages apply in rare cases where the at-fault driver acted with extreme recklessness or intentional misconduct. They are not tied to your actual losses. Most car accident claims do not involve punitive damages, so the focus here stays on economic and non-economic losses, which are the categories that affect nearly every accident victim.

How to calculate economic damages: documenting actual financial losses

The damage assessment process for economic losses follows a straightforward sequence. Every step depends on documentation, and gaps in your records give insurers a reason to reduce your payout.

-

Gather every medical bill. Request itemized statements from every provider, not summary totals. Itemized medical bills and provider credentials carry more weight than a single-page summary when proving medical expenses. Include bills from the emergency room, specialists, imaging centers, pharmacies, and any ongoing therapy.

-

Project future medical costs. Ask your treating physician to document expected future treatment in writing. Future medical expenses are recoverable, but only if a qualified provider puts them on record. A letter from your doctor estimating six months of physical therapy at a specific cost per session gives your claim a concrete number to work with.

-

Calculate lost wages precisely. Pull your pay stubs from the three months before the accident to establish your baseline income. Multiply your daily or weekly rate by the number of days you missed work. If you are self-employed, use tax returns and client invoices to show your average earnings. For partial work loss, calculate the difference between what you earned and what you would have earned at full capacity.

-

Document lost earning capacity separately. If your injuries affect your long-term ability to work, this calculation goes beyond missed paychecks. A vocational expert or forensic economist can project the lifetime income gap. This figure often represents the largest single component of a serious injury claim.

-

Get multiple repair estimates. Obtain at least two written estimates from licensed body shops for vehicle damage. Insurance adjusters will use their own estimate, which may be lower. Having independent estimates on file gives you a basis to dispute a low offer.

-

Record every out-of-pocket expense. Keep a running log of mileage to medical appointments, parking fees, rideshare costs, and any home care you paid for. These amounts add up and are fully recoverable.

-

Show your mitigation efforts. Failure to mitigate damages can reduce your recoverable amounts. Document every step you took to limit your losses: following your doctor’s treatment plan, returning to modified work when cleared, and seeking alternative income when possible. Insurers look for reasons to cut claims, and a lack of mitigation evidence is one of the easiest arguments they use.

Pro Tip: Open a dedicated folder on your phone and scan every receipt the same day you receive it. Faded thermal paper receipts from pharmacies become unreadable within months, and a missing $400 prescription bill is $400 you cannot recover.

How to estimate non-economic damages like pain and suffering

Non-economic damages do not have a fixed formula set by law. Two methods dominate settlement negotiations: the multiplier method and the per diem method. Neither is mandated by statute. Both are tools used to reach a number that a jury or insurer might accept.

The multiplier method

The multiplier method takes your total economic damages and multiplies them by a factor that reflects the severity of your injuries. The scale typically runs from 1.5 to 5, with 1.5 applied to minor soft-tissue injuries and 5 reserved for catastrophic or permanent harm.

| Injury severity | Typical multiplier range | Example economic damages | Estimated non-economic damages |

|---|---|---|---|

| Minor (soft tissue, short recovery) | 1.5x | $10,000 | $15,000 |

| Moderate (fractures, surgery needed) | 2x–3x | $40,000 | $80,000–$120,000 |

| Severe (permanent disability) | 4x–5x | $100,000 | $400,000–$500,000 |

The multiplier is a negotiation tool, not a legal entitlement. What moves the multiplier up is evidence quality. Strong medical records, a consistent treatment history, and testimony from your doctor and family members all push the number higher. Weak or inconsistent records push it lower.

The per diem method

The per diem method assigns a daily dollar value to your pain and suffering, then multiplies it by the number of days you experienced impairment. A common starting point is your daily earnings rate. For example, if you earn $220 per day and your recovery lasted 180 days, the per diem calculation produces $39,600 in non-economic damages.

The per diem approach works best for injuries with a clear end date. It becomes harder to apply when impairment is permanent or fluctuates over time.

Pro Tip: Keep a daily pain journal from the day of the accident. Write two or three sentences each day about how your injuries affected your sleep, your ability to care for your children, or your capacity to do your job. That journal becomes direct evidence supporting a higher multiplier or a longer per diem period.

What evidence supports non-economic claims

Non-economic damages depend on the volume and quality of evidence, not a fixed formula. The most persuasive evidence includes:

- Detailed medical records showing the progression and treatment of your injuries

- A pain journal documenting daily limitations

- Statements from family members, coworkers, or friends describing changes in your behavior and abilities

- Testimony from your treating physician about the impact on your quality of life

You can learn more about what counts as pain and suffering under Colorado law and how courts evaluate these claims.

How to estimate losses for income disruption and repair costs

The but-for income analysis

Lost income calculations use a “but-for” baseline: what you would have earned if the accident had never happened. Lost income calculations compare actual earnings to that baseline, then adjust for costs you avoided because you were not working.

For example, a self-employed contractor who normally earns $5,000 per month but earned $1,500 during recovery has a gross income gap of $3,500. From that, you subtract costs you did not incur because you were not working, such as fuel, materials, or subcontractor fees. The result is your net lost income. This distinction matters because only incremental costs tied to lost work should reduce your damages, not fixed overhead like rent or insurance that you paid regardless.

Defining the damage period clearly

Proper damage period definition is critical to any income loss claim. Adjusters and defense attorneys scrutinize whether your impairment truly began with the accident and whether it ended when your medical records say it did. Vague start and end dates invite disputes. Pin your damage period to specific medical events: the date of the accident, the date of surgery, the date your doctor cleared you to return to work.

Sources for credible repair cost estimates

Vehicle repair costs are among the most disputed components of a car accident claim. Use these sources to build a defensible estimate:

- Licensed body shops: Get at least two written estimates from shops that specialize in your vehicle’s make. Dealership service centers often carry more credibility with insurers.

- Total loss valuation tools: If your vehicle is totaled, reference published valuation guides that insurers themselves use to establish fair market value.

- Diminished value claims: Even after repairs, a vehicle that has been in an accident is worth less on the resale market. Colorado allows diminished value claims, and this loss is separate from repair costs.

| Repair cost source | Credibility with insurers | Notes |

|---|---|---|

| Licensed body shop estimate | High | Get two or more for comparison |

| Dealership service center | High | Especially for newer or luxury vehicles |

| Online valuation tools | Moderate | Useful for total loss disputes |

| Verbal or informal quotes | Low | Not accepted without written documentation |

Common pitfalls to avoid

Failing to document the damage period precisely is the most common error in income loss claims. The second most common mistake is confusing total costs with incremental costs when calculating lost profits for self-employed claimants. A third pitfall is accepting the insurer’s first repair estimate without getting an independent assessment. Each of these errors directly reduces your recoverable amount. Thorough injury documentation from day one is the single most effective way to avoid all three.

What I’ve learned after a decade of fighting these claims

After more than ten years handling personal injury cases in Colorado, and before that working as a claims adjudicator for the federal government, I can tell you the single biggest mistake accident victims make: they underestimate how quickly evidence disappears.

Surveillance footage gets overwritten within 30 days. Witnesses forget details within weeks. Medical records from urgent care clinics sometimes take months to retrieve. By the time a client comes to me three months after an accident, critical evidence is already gone. The damage assessment process is not something you can start after you feel better. It starts the day of the crash.

The second thing I have seen consistently is that clients accept the insurer’s first offer without understanding what their non-economic damages are worth. The multiplier method is a negotiation tool, not a ceiling. I have seen cases where the initial offer reflected a 1.5x multiplier, and the final settlement reflected a 3x multiplier, simply because we built a stronger evidence file. The quality of your documentation does not just support your claim. It determines the number you walk away with.

I also want to address the mitigation requirement directly, because it surprises people. You have a legal obligation to take reasonable steps to limit your own losses. That means following your doctor’s orders, attending every appointment, and returning to work in a modified capacity when your physician clears you. Insurers look for evidence that you did not do these things. When they find it, they use it to cut your claim. Document your compliance with the same discipline you document your losses.

If your claim involves significant lost income, a permanent injury, or a disputed liability situation, get a professional involved early. The cost of a consultation is trivial compared to the difference between a low settlement and a fair one.

— Ryan

How Stubbornattorney can support your damage claim

Calculating your losses after a car accident is one thing. Getting a fair settlement from an insurer who has every incentive to pay less is another. Stubbornattorney, the practice of Ryan Malnar, has settled hundreds of injury cases and recovered millions of dollars for Colorado accident victims. Ryan’s background as a former federal claims adjudicator means he knows exactly how insurers evaluate claims and where they look for weaknesses. If you want to understand what your case is actually worth, start with a free case review and get a clear picture of your options. You can also review common personal injury case examples to see how cases like yours have been handled.

FAQ

What does estimating damages mean after a car accident?

Estimating damages means calculating both your economic losses, such as medical bills and lost wages, and your non-economic losses, such as pain and suffering, to determine the total compensation you can pursue from an insurer or in court.

What is the multiplier method for pain and suffering?

The multiplier method multiplies your total economic damages by a factor between 1.5 and 5, based on injury severity and evidence strength. It is a negotiation tool used in settlements, not a formula set by law.

How do I calculate lost wages after a car accident?

Multiply your daily or weekly earnings rate by the number of days you missed work. Self-employed claimants should use tax returns and client invoices to establish a baseline, then subtract only the incremental costs they avoided by not working.

What is the per diem method for non-economic damages?

The per diem method assigns a daily dollar value to your pain and suffering, often based on your daily earnings, and multiplies it by the number of days you experienced impairment. For example, $220 per day over 180 days of recovery produces $39,600 in non-economic damages.

Does failing to follow medical advice reduce my damages?

Yes. Failure to mitigate damages can reduce your recoverable amount. Insurers and courts expect you to follow your doctor’s treatment plan and take reasonable steps to limit your losses. Documenting your compliance protects your claim from reduction.