What Is Liability Insurance? A Guide for Owners

Liability insurance is defined as a contract that pays for your legal responsibilities when you cause bodily injury or property damage to another person. The policy covers legal defense costs, settlements, and court judgments, so you do not pay those bills out of pocket. Costs for major accidents can quickly climb into six figures, which means a single lawsuit can wipe out savings, home equity, or retirement accounts without this protection. Both individuals and business owners carry liability coverage, though the specific policy type depends on the risk they face. Understanding how this coverage works is the first step toward protecting everything you have built.

What is liability insurance and what types exist?

Liability insurance is the formal industry term for third-party coverage. It protects you from claims made by other people, not from your own injuries or losses. That distinction separates it from health insurance, property insurance, and disability coverage, all of which protect the policyholder directly.

The most common types break down by who needs them and what they cover.

For businesses:

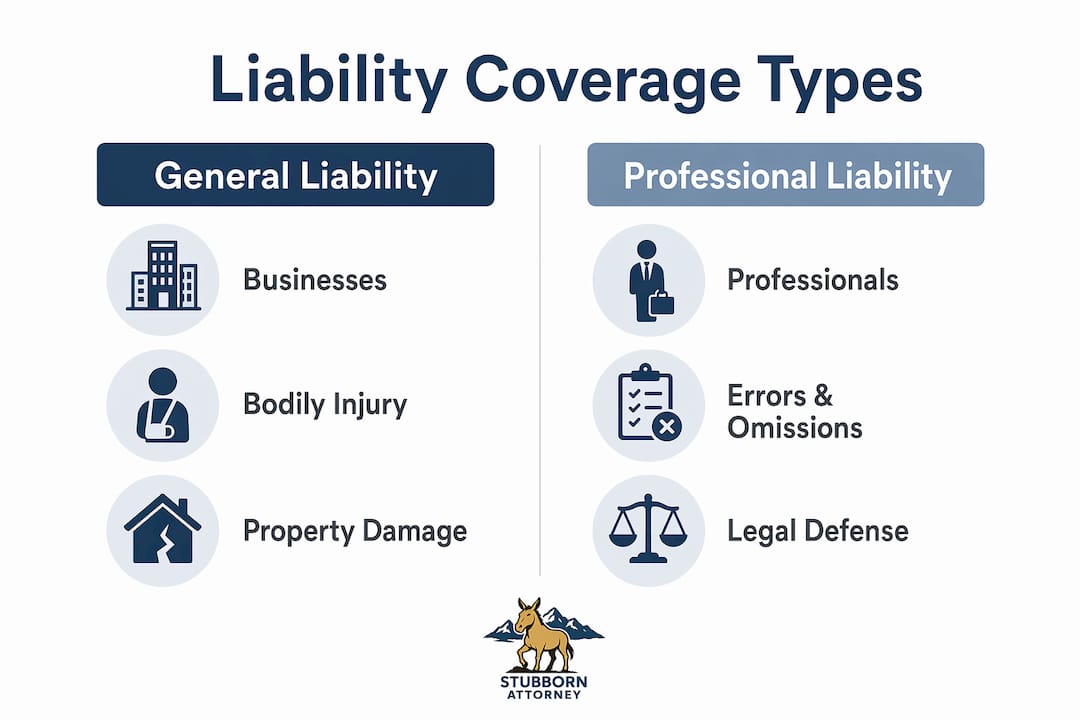

- General liability insurance covers bodily injury, property damage, and advertising injury claims. Coverage applies on-site and after project completion, which means a contractor can still face a covered claim months after finishing a job.

- Professional liability insurance, also called errors and omissions (E&O), covers claims that your advice or service caused financial harm. Doctors, lawyers, accountants, and consultants typically carry this.

- Product liability insurance covers injuries or damage caused by a product your business manufactured or sold. You can read more about how product liability claims work and what rights injured parties hold.

For individuals:

- Personal liability coverage comes bundled inside most homeowners and renters insurance policies. It pays if a guest is injured on your property or if you accidentally damage someone else’s belongings.

- Auto liability insurance is mandatory in nearly all U.S. states. It covers the other driver’s injuries and vehicle damage when you cause a crash.

| Coverage type | Who carries it | What it covers |

|---|---|---|

| General liability | Businesses | Bodily injury, property damage, advertising injury |

| Professional liability | Service providers | Negligent advice or service errors |

| Product liability | Manufacturers, retailers | Injuries from defective products |

| Personal liability | Homeowners, renters | Injuries or damage caused by the policyholder |

| Auto liability | Drivers | Other party’s injuries and vehicle damage |

Pro Tip: General liability is often required in commercial leases. Check your lease agreement before signing. Showing up without coverage can void the contract.

How does liability insurance work when a claim is made?

Liability coverage is triggered by negligence or an accident, not by intent. When someone claims you caused them harm, the process follows a clear sequence.

- An incident occurs. A customer slips in your store, a driver rear-ends another car, or a client claims your advice cost them money.

- A claim is filed. The injured party notifies your insurer directly or files a lawsuit against you.

- The insurer investigates. Your insurance company assigns a claims adjuster who reviews evidence, interviews witnesses, and evaluates the claim’s validity.

- Legal defense begins. Your insurer covers defense costs even if the claim is false or exaggerated. You do not pay attorney fees out of pocket while the case is active.

- Settlement or judgment. If the claim is valid, the insurer pays the settlement or court judgment up to your policy limit.

One critical detail: liability insurance never covers intentional acts or criminal behavior. If you deliberately damage property or assault someone, the insurer will not defend you or pay the claim. Coverage is strictly for accidents and negligence.

Policy limits define the maximum the insurer will pay. A policy with a $1,000,000 per-occurrence limit pays up to that amount for a single incident. If a court awards $1,500,000, you owe the remaining $500,000 personally. Excess judgments become personal debt, putting assets like your home or retirement savings at direct risk. Understanding how liability is established in a claim helps you see why adequate limits matter from the start.

Pro Tip: Ask your insurer about umbrella liability policies. An umbrella policy adds a layer of coverage above your existing limits, often for a modest annual premium, and it can be the difference between a manageable loss and financial ruin.

What are the key benefits and limitations of liability insurance?

The primary benefit of liability insurance is financial protection from lawsuits you cannot predict. A single slip-and-fall claim, a car accident, or a professional error can generate legal costs that no individual or small business can absorb without help.

Core benefits:

- Asset protection. Insurance prevents forced liquidation of personal assets during legal actions. Your home, savings, and business equipment stay protected while the insurer handles the claim.

- Business continuity. A lawsuit does not have to shut you down. The insurer manages the legal process, so you keep operating while the case resolves.

- Credibility with clients and partners. Carrying proper liability coverage demonstrates professional responsibility to clients, landlords, and vendors. Many contracts require proof of coverage before work begins.

- Legal defense at no extra cost. Defense attorney fees are covered under the policy, even when the claim has no merit.

“Liability insurance acts as a financial safety net against life’s unexpected moments, preserving personal assets and keeping businesses running when legal claims arise.” — Understanding Liability Insurance Benefits

Limitations you need to know:

- Policy limits cap your protection. Any judgment above your limit becomes your personal responsibility.

- Exclusions create gaps. Intentional acts, criminal activity, and certain professional errors may fall outside standard general liability coverage.

- One policy rarely covers everything. Combining multiple liability policies is the standard approach for avoiding coverage gaps, especially when professional negligence and general incidents both represent real risks.

- Completed operations claims can surprise you. A contractor who finishes a job in march may face a claim in november if the work later causes harm. Completed operations coverage extends protection to those delayed claims.

A common misconception is that general liability covers everything. It does not. A business owner who gives bad financial advice needs professional liability coverage, not just general liability. Matching the right policy to the right risk is the only way to close those gaps.

How can you use liability insurance to manage risk effectively?

Selecting the right coverage starts with an honest assessment of your actual risk exposure. A freelance graphic designer faces different risks than a restaurant owner or a general contractor. Tailoring coverage to actual risk helps avoid both coverage gaps and unnecessary premiums.

Practical steps for individuals and business owners:

- Audit your risk profile. List every activity that could result in injury or property damage to a third party. Include your home, vehicle, business operations, and any products you sell.

- Set limits based on your assets. Your coverage limit should be at least equal to your total net worth. If a judgment exceeds your limit, your personal assets cover the rest.

- Read the exclusions section. Every policy lists what it will not cover. Read that section before you sign, not after a claim is denied.

- Request a certificate of insurance. This document proves your coverage to clients, landlords, and general contractors. Carrying one builds trust and satisfies contractual requirements before work begins.

- Review your policy annually. Your risk profile changes as your business grows, your home value rises, or your family situation shifts. A policy that fit three years ago may leave you underinsured today.

Pro Tip: If you are a business owner, ask your insurer whether your policy includes completed operations coverage. Many standard policies require you to add it separately, and claims from finished work are among the most common surprises business owners face.

Integrating liability coverage with other policies creates a complete safety net. Pair general liability with a commercial property policy, a professional liability policy, and a commercial auto policy if your business uses vehicles. Individuals should confirm that their homeowners or renters policy includes personal liability coverage and that their auto policy meets state minimums. You can review common personal injury case examples to see the range of situations where liability coverage becomes the deciding factor between financial recovery and financial loss.

The most common pitfall is buying the cheapest policy without checking the limits. A $300,000 general liability policy sounds substantial until a jury awards $750,000. Buy the coverage your actual exposure demands, not the minimum that satisfies a contract requirement.

What I have learned about liability insurance after a decade in injury law

After more than a decade representing injured clients in Colorado, I have watched the same pattern repeat itself. The person on the other side of a lawsuit, whether an individual homeowner or a small business owner, almost always underestimated their liability exposure before the incident occurred. They assumed their existing coverage was enough, or they assumed a claim of that size would never happen to them.

The financial reality is blunt. A lawsuit does not care about your intentions. It cares about what a jury decides you owe. I have seen people lose home equity and retirement savings because their policy limit was set years ago and never updated. I have seen small businesses close because a single judgment exceeded their coverage by a margin they never planned for.

What I tell every client who asks about liability coverage is this: think of it the way I think about a sure-footed mule on a steep Colorado trail. The mule does not wait until the ledge crumbles to find solid ground. It reads the terrain before each step. Liability insurance works the same way. You buy it before the fall, not after.

The other mistake I see constantly is treating liability insurance as a checkbox. People buy the minimum required by a lease or a state law and stop there. That approach protects the landlord or the state, not you. Sit down with an independent insurance agent, review your actual assets, and set limits that reflect what you stand to lose. That is the only version of this coverage that actually protects you.

— Ryan

Liability claims and legal support in Colorado

When a liability claim turns into a lawsuit, the legal process moves faster than most people expect. Stubbornattorney represents injured victims across Colorado and has recovered millions of dollars in settlements for people navigating exactly these situations. Ryan Malnar spent years as a federal claims adjudicator before becoming a personal injury attorney, which means he understands how insurers evaluate claims from both sides of the table. If you are dealing with a liability dispute, a denied claim, or a lawsuit that has exceeded your coverage, a free case review gives you a clear picture of your options. Read through common personal injury cases to see how these claims typically unfold, or contact Stubbornattorney directly for a free personal injury consultation.

FAQ

What is liability insurance in simple terms?

Liability insurance is a policy that pays for legal costs, settlements, and judgments when you are found responsible for injuring someone or damaging their property. It protects your personal and business assets from being seized to satisfy a court judgment.

Do I need liability insurance if I already have health insurance?

Yes. Health insurance covers your own medical bills. Liability insurance covers the costs you owe to other people when you cause them harm. The two policies serve completely different purposes.

What does liability insurance not cover?

Liability insurance does not cover intentional acts or criminal behavior. It also does not cover your own injuries, damage to your own property, or claims that fall outside the specific policy type you carry.

How much liability insurance coverage do I actually need?

Coverage limits should match or exceed your total net worth, because any judgment above your policy limit becomes personal debt. Business owners with significant assets or high-risk operations should consider umbrella policies for additional protection.

Is liability insurance required by law?

Auto liability insurance is required by law in nearly all U.S. states. General liability insurance for businesses is not always legally mandated, but it is frequently required by commercial leases and client contracts before work can begin.