The Role of Insurance Adjuster in Personal Injury Claims

An insurance adjuster is the professional who investigates claims and decides how much an insurer will pay. Understanding the role of insurance adjuster in your personal injury case is not optional knowledge. It is the difference between accepting a low first offer and walking away with a fair settlement. Adjusters work for the insurance company, not for you. They follow policy terms, state regulatory requirements, and internal reserve-setting procedures designed to protect the insurer’s bottom line. Knowing how they operate gives you a real advantage.

What is the role of an insurance adjuster?

The role of an insurance adjuster is to evaluate claims on behalf of the insurer and determine the appropriate payout within policy limits. The industry term for this professional is “claims adjuster,” though the titles are used interchangeably. Their primary obligation runs to the insurance company, not to the person filing the claim.

Adjusters are bound to their insurer, working to minimize what the company pays out. That single fact reshapes every conversation you will ever have with one. Many claimants walk into their first adjuster call expecting a neutral fact-finder. They are not neutral. They are trained evaluators with a financial target.

The claims adjuster’s job begins the moment a claim is filed. They gather evidence, review your policy, assess damages, and set a reserve, which is an internal dollar estimate of what the claim will cost the insurer. That reserve number influences every negotiation that follows. The insurance claims process moves fast, and adjusters are experienced at it. Most claimants are not.

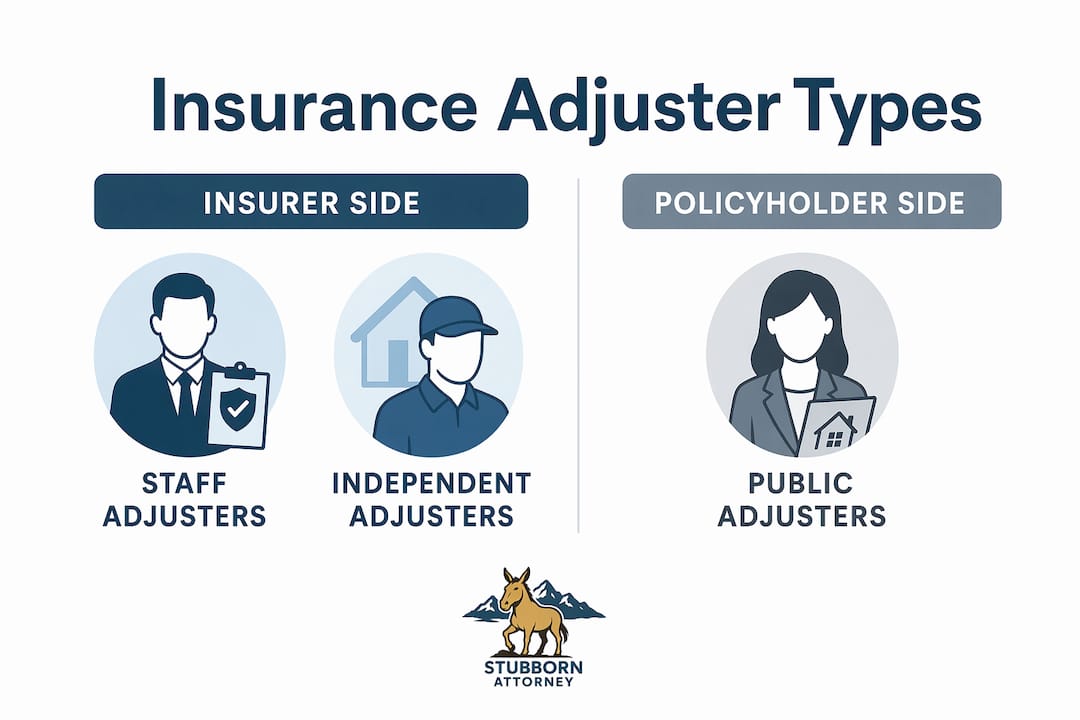

What types of insurance adjusters exist and how do their roles differ?

Insurance adjusters fall into three categories: staff adjusters, independent adjusters, and public adjusters. Each type has different incentives, different employers, and a different relationship to your claim.

Staff adjusters

Staff adjusters are full-time employees of the insurance company. They handle claims daily, know their employer’s policies inside out, and are evaluated on claim closure speed and cost control. Their loyalty is entirely to the insurer. You will encounter staff adjusters most often when dealing with your own insurance company or the at-fault party’s insurer after a standard accident.

Independent adjusters

Independent adjusters are contractors hired by insurers, typically during high-volume periods like natural disasters or catastrophic events. They are paid per claim, which creates pressure to close files quickly. Their incentives align with the insurer’s, not yours. The quality of their investigation can vary more than a staff adjuster’s because they lack the same institutional oversight.

Public adjusters

Public adjusters work exclusively for the policyholder. They are the only adjuster type whose financial interest aligns with yours. Public adjuster fees typically range from 10–15% of the final settlement, paid by the claimant. That fee structure means they are motivated to maximize your payout. Public adjusters can write competing damage assessments and negotiate directly with the insurer’s adjuster, often increasing settlements enough in complex cases to justify their cost.

| Adjuster type | Who employs them | Primary goal | Cost to claimant |

|---|---|---|---|

| Staff adjuster | Insurance company | Minimize insurer payout | None |

| Independent adjuster | Insurer (contract) | Close claims efficiently | None |

| Public adjuster | Policyholder | Maximize claimant settlement | 10–15% of settlement |

Pro Tip: If your property damage claim is large or disputed, a public adjuster’s competing scope of loss can shift the negotiation significantly. For personal injury claims, an attorney typically provides stronger protection and negotiates from a position of legal authority.

What are the main duties and responsibilities of an insurance adjuster?

The core duties of a claims adjuster cover the full arc of a claim, from the initial incident report to the final settlement check. Understanding each duty helps you anticipate what the adjuster is doing and why.

- Investigate the incident. Adjusters review police reports, medical records, photographs, and witness statements to verify that the claim is valid and that the facts support the coverage being requested.

- Evaluate policy coverage. They read your policy carefully, identifying exclusions, coverage limits, and conditions that could reduce or eliminate the insurer’s obligation to pay.

- Set claim reserves. Early in the process, adjusters assign a dollar reserve to your file. This estimate shapes the insurer’s financial exposure and can anchor negotiations if your documented damages later exceed it.

- Arrange damage inspections. For vehicle or property damage, adjusters coordinate with contractors, repair shops, or independent experts to get repair estimates. In personal injury cases, they review medical bills and treatment records.

- Negotiate settlements. The adjuster’s negotiation goal is to close your claim at the lowest defensible number within policy limits. Their first offer is almost always below what the claim is actually worth.

- Document everything. Adjusters maintain detailed file notes on every conversation, every piece of evidence, and every decision. Those notes can be used against you if your statements are inconsistent.

Adjusters set reserves early, and those numbers can lock in a low valuation if your initial information is incomplete or contradictory. This is why the evidence you provide, and the statements you make, matter from day one. A strong, well-documented claim forces a higher reserve and a better opening offer.

Pro Tip: Before any adjuster contact, gather your medical records, bills, photos, and a written account of the incident. A complete evidence file at the start of the process gives the adjuster less room to undervalue your claim.

The claims process is a negotiation that starts the moment you file. The first offer is a starting position, not a final answer. Evidence-backed pushback is the standard path to a fair result.

How should you effectively interact with insurance adjusters?

Your legal obligations differ depending on which adjuster you are speaking to. You are required to cooperate with your own insurer’s adjuster because your policy contract says so. You have no such obligation with the opposing party’s insurer. Many claimants confuse these two situations and give far more information than they need to, which damages their claim.

Here is a clear list of what to do and what to avoid when dealing with insurance adjusters:

- Do confirm basic facts only. Your name, contact information, and the date and location of the accident are appropriate to share with an adverse adjuster. Nothing more is required.

- Do not speculate about fault. Saying “I might have been going a little fast” or “I didn’t see them coming” can be used to reduce your settlement. Stick to what you know for certain.

- Do not give a recorded statement to the adverse insurer without an attorney present. Adjusters are trained to elicit statements that reduce claim value. You are not obligated to provide one.

- Do document every contact. Write down the adjuster’s name, the date, and a summary of what was discussed after every call or meeting.

- Do not accept the first offer without review. The initial settlement offer is almost always below the actual value of your claim.

- Do get legal representation early. An attorney manages adjuster communications on your behalf, removing the risk of accidental statements that harm your case.

- Do not discuss your injuries as minor or improving. Medical conditions evolve. Statements made early can contradict later diagnoses and reduce your compensation.

Adjusters use rapport-building tactics to lower your guard. A friendly, conversational tone is a professional technique, not a sign of goodwill. The notes from that friendly call go straight into your claim file. Treat every interaction as a formal proceeding, even when it does not feel like one.

Pro Tip: If an adjuster calls you unexpectedly, you are not required to speak with them on the spot. It is entirely appropriate to say, “I will call you back,” and use that time to consult an attorney before responding.

You can learn more about protecting your position by reviewing this car accident injury checklist before your first adjuster contact.

When should you hire a public adjuster or attorney for your claim?

Not every claim requires professional representation, but the cases where it matters most are easy to identify. The more complex or disputed your claim, the stronger the case for bringing in a professional.

Situations where a public adjuster adds clear value:

- Large property damage claims where the insurer’s repair estimate is significantly lower than contractor quotes

- Claims involving multiple coverage types or disputed policy exclusions

- Catastrophic loss situations where the insurer’s adjuster is managing dozens of files simultaneously

For personal injury claims, an attorney is almost always the better choice over a public adjuster. Attorneys negotiate from a position of legal authority. They can file suit, compel discovery, and present your case to a jury if necessary. A public adjuster cannot do any of those things.

Legal counsel significantly strengthens your negotiating position because adjusters know that an attorney-represented claimant is prepared to litigate. That knowledge alone shifts the dynamic. Insurers settle faster and for more money when they know the alternative is a courtroom.

| Claim type | Best professional support | Key benefit |

|---|---|---|

| Large property damage | Public adjuster | Competing damage scope, fee-based motivation |

| Disputed personal injury | Personal injury attorney | Legal authority, litigation threat, full damages recovery |

| Minor fender-bender, no injury | Self-represented | Cost-effective for low-value, clear-liability claims |

| Complex multi-party accident | Personal injury attorney | Manages multiple insurers, preserves all legal rights |

The cost-benefit calculation for a public adjuster depends on the gap between the insurer’s offer and the actual loss. Public adjuster fees of 10–15% are worth paying when the settlement increase exceeds that percentage. For personal injury claims, most attorneys work on contingency, meaning you pay nothing unless you win. That structure removes the financial barrier to getting proper representation.

Steps to decide whether to hire professional help:

- Assess whether the insurer’s offer covers your documented losses

- Determine whether liability is disputed or clear

- Consider whether your injuries are serious or ongoing

- Evaluate whether the insurer is delaying, denying, or undervaluing your claim

If any of those factors point toward a dispute, professional representation is the right call. You can review how attorneys fight insurance companies in Colorado to understand what that representation looks like in practice.

What I have learned from both sides of the claims table

I spent years as a claims adjudicator for the federal government before becoming a personal injury attorney. That experience gave me a view of the claims process that most lawyers simply do not have. I have sat in the adjuster’s chair. I know exactly how claims are evaluated, how reserves are set, and how statements are used to justify low offers.

The most consistent mistake I see claimants make is treating the adjuster like a partner. They answer every question, share every detail, and assume that being cooperative will be rewarded with a fair offer. It will not. Cooperation with your own insurer is a contractual requirement. Cooperation with the adverse insurer is a choice, and it is usually a costly one.

The second mistake is waiting too long to get an attorney involved. By the time most claimants call me, they have already given a recorded statement, accepted a partial payment, or made an offhand comment that the adjuster has documented. Those early missteps are hard to undo. Early legal intervention does not just protect your claim. It changes the entire dynamic of the negotiation.

My advice is direct: treat the claims process as a negotiation from the first phone call. Document everything. Say less than you think you need to. And if your injuries are serious or liability is disputed, get an attorney before you speak to any adjuster. The adjuster has done this thousands of times. You have not. That experience gap is real, and it costs claimants money every day.

— Ryan

How Stubbornattorney can help you face insurance adjusters

Stubbornattorney, the brand home of Malnar Injury Law, represents only injured victims across Colorado. Ryan Malnar’s background as both a former claims adjudicator and a personal injury attorney means the firm understands exactly how insurers evaluate and undervalue claims. That inside knowledge shapes every negotiation. Stubbornattorney has settled hundreds of injury cases and recovered millions of dollars for clients who came in facing low initial offers and aggressive adjuster tactics. A free case evaluation costs you nothing and gives you a clear picture of what your claim is actually worth. If you have been injured and an adjuster has already made contact, review common personal injury case examples to see how similar claims have been handled, or go directly to the personal injury services page to start your free consultation today.

FAQ

What does an insurance adjuster actually do?

An insurance adjuster investigates claims, evaluates policy coverage, and negotiates settlements on behalf of the insurer. Their goal is to close claims at the lowest defensible amount within policy limits.

Do I have to talk to the other driver’s insurance adjuster?

You are not legally required to cooperate with the opposing party’s insurer. Your obligation to cooperate applies only to your own insurer under your policy contract.

Why do insurance adjusters negotiate instead of paying the full claim?

Adjusters negotiate because minimizing payouts is their core function. The claims process is a negotiation from the start, and the first offer is a starting position, not a final answer.

Can an attorney stop an adjuster from contacting me directly?

Yes. Once you retain an attorney, the adjuster must direct all communications through your lawyer. This removes the risk of accidental statements harming your claim.

When is hiring a public adjuster worth the cost?

A public adjuster is worth the 10–15% fee when the gap between the insurer’s offer and your actual documented loss is large enough to justify it. For personal injury claims, a contingency-fee attorney typically provides stronger protection at no upfront cost.