Insurance Claim Workflow: Your Step-by-Step Guide

Filing an insurance claim after an accident is one of those things nobody prepares for until they’re already in it. You’re stressed, possibly injured, dealing with damaged property, and suddenly you need to understand a process that insurance companies navigate every day but rarely explain clearly to you. Knowing the insurance claim workflow before you need it, or learning it quickly after an accident, makes a real difference in how fast your claim gets resolved and how much you actually receive. This guide covers exactly what to do, in what order, with no guesswork required.

Table of Contents

- What you need before starting an insurance claim

- Step-by-step insurance claim workflow for accident claims

- Common pitfalls that slow or kill your claim

- Understanding timelines in the claim resolution workflow

- What I have learned from a decade on both sides of claims

- When your claim needs more than a workflow

- FAQ

What you need before starting an insurance claim

Most claims run into trouble not because of what happens at the insurance company, but because of what the claimant failed to do in the first 24 to 72 hours. Getting organized before you pick up the phone is the single most impactful step you can take.

What to gather at the accident scene

If you are physically able, collect as much information as possible before leaving the scene. For auto accidents, that means photos of every vehicle involved, photos of the road conditions, the other driver’s contact and insurance information, and names and phone numbers of any witnesses. The same principle applies to home incidents: photograph damage before any cleanup begins, because the original state of the damage matters significantly to adjusters.

For auto claims, report within 48 to 72 hours to keep the process moving efficiently. Waiting longer than that introduces gaps in evidence and can give insurers a reason to delay evaluation.

Here is a quick-reference checklist of what to gather:

- Date, time, and exact location of the incident

- Photos and video from multiple angles

- Police or incident report number (request a copy)

- Names, contact information, and insurance details for all parties

- Witness names and phone numbers

- Any visible injuries documented with photos

- Receipts for any immediate expenses tied to the incident (hotel, tow, emergency medical)

For home or property claims, you will generally need to submit a proof of loss form listing all damaged items with estimated values, supporting photos, and any receipts within roughly 30 days.

Reviewing your policy before you file

Pull out your insurance policy and read the sections on coverage limits, deductibles, and deadlines. Most people skip this step and later discover that something they expected to be covered is excluded, or that they missed a reporting deadline buried in the fine print. Pay attention to any mandatory reporting windows, because missing them can void your claim entirely.

Early insurer notification allows your insurer to begin policy review and assign an adjuster faster, which directly speeds up your claim. Knowing your deductible amount also helps you calculate whether filing even makes sense for smaller incidents.

Pro Tip: Create a physical or digital folder before you make your first call to the insurer. Include every photo, the police report, your policy number, and a written timeline of what happened. Organized claimants consistently move through the process faster than those who piece together documents on request.

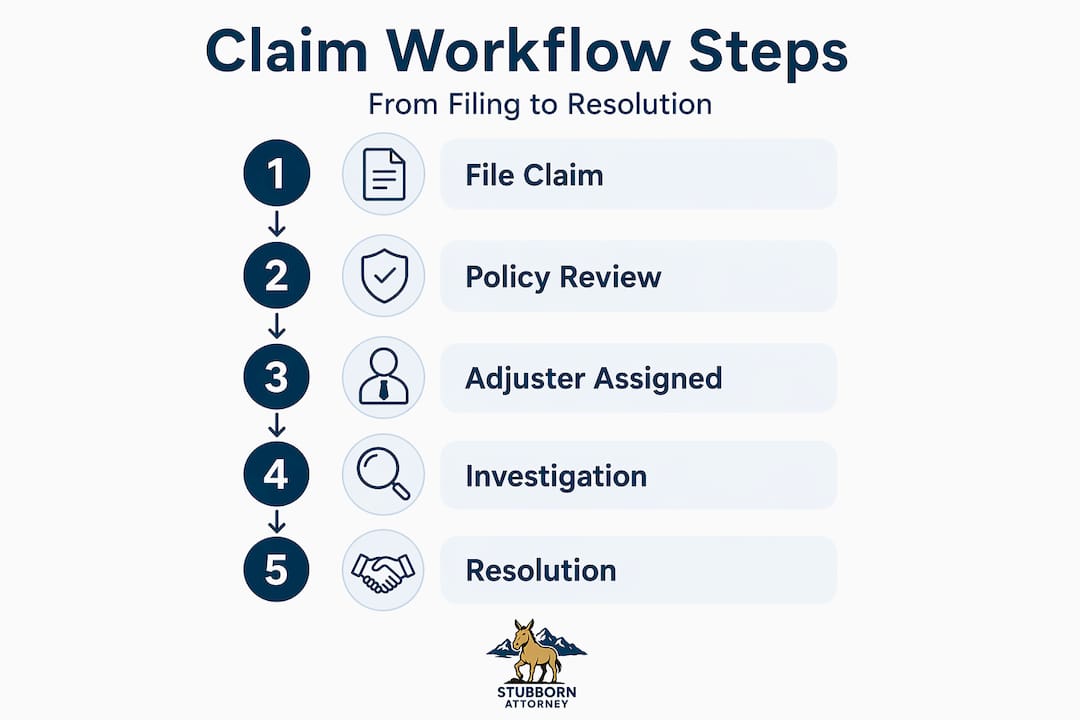

Step-by-step insurance claim workflow for accident claims

Understanding the exact sequence of the claims processing system removes the anxiety of not knowing what comes next. Every insurer has its own forms and portals, but the underlying process follows the same logic across auto, home, and personal injury claims.

The standard workflow, step by step

-

File the first notice of loss (FNOL). This is your official report to the insurer. It triggers the entire workflow. A complete, well-structured FNOL reduces back-and-forth and speeds adjuster assignment. Do not drip information out over multiple calls. Submit everything you have in one organized report.

-

Receive claim number and adjuster assignment. After your FNOL, you will get a claim number and the name of the adjuster assigned to your case. Write both down. Every future communication should reference your claim number.

-

Submit documentation. Your adjuster will send a list of required documents. Submit them together rather than one at a time. For complex property claims, room-by-room photos with contractor estimates organized to match how an adjuster reviews a file will reduce unnecessary delays.

-

Damage inspection. The adjuster will arrange an inspection of the damaged vehicle, property, or, in injury claims, will review medical records. For auto claims, this may involve an in-person inspection or a virtual photo review. Do not authorize permanent repairs before the inspection is complete.

-

Review and investigation. The insurer verifies your documentation, checks for coverage, and determines liability. This is where disputes or requests for additional information most commonly occur.

-

Claim decision. The insurer accepts, partially accepts, or denies your claim. If accepted, they issue a settlement offer. If denied, you have the right to appeal.

-

Settlement and payment. Once you agree to the settlement and pay your deductible, the insurer issues payment. For auto repairs, payment often goes directly to the repair shop.

Workflow variations by claim type

| Claim Type | Key Difference | Typical Additional Requirement |

|---|---|---|

| Auto | Inspection of vehicle required | Repair shop estimates or insurer referral |

| Home/Property | Proof of loss form required | Itemized inventory with photos and receipts |

| Personal Injury | Medical records review | Medical authorization forms, treatment timeline |

| Health Insurance | ERISA deadlines apply | Explanation of Benefits review, provider billing |

Health insurance claims operate under specific federal timelines. Urgent claims must be resolved within 72 hours, while non-urgent claims have a 15 to 30 day decision window under ERISA rules. That is a meaningfully faster timeline than most people expect.

Pro Tip: Ask your adjuster at the very first contact: “What documents do you need, and in what format?” Adjusters work through dozens of files simultaneously. The claimants who make the adjuster’s job easier by providing exactly what is needed get faster responses every time.

For a detailed breakdown of what evidence matters most in Colorado accident claims, the Colorado car accident legal checklist from Stubbornattorney walks through each required element with real specificity.

Common pitfalls that slow or kill your claim

Even when you follow the steps correctly, certain mistakes can throw your claim off track for weeks. Here are the ones that show up most often in insurance claims management.

The most frequent mistakes claimants make

- Late reporting. Every policy has a reporting deadline. Some are as short as 30 days for certain incident types. Missing the window gives your insurer grounds to deny based on late notice alone.

- Incomplete initial report. Submitting a partial FNOL and filling in details later forces the adjuster to pause the file repeatedly. Each pause adds days or weeks to your timeline.

- Failing to document communication. Most claim disputes come down to “he said, she said” situations. A single-threaded communication log that captures every call, email, and written recap dramatically reduces this risk. After each phone call with your adjuster, send a brief email summarizing what was discussed and agreed to.

- Misreading coverage limits. A common shock for claimants is discovering mid-claim that their policy covers less than they assumed. Read the declarations page before you file, not after.

- Accepting the first settlement offer too quickly. Insurance companies are businesses. Their first offer is rarely their best. You have the right to negotiate or dispute the figure, especially when medical treatment is ongoing.

The most expensive thing most people do in the claims process is move too fast. They accept the first number because they want it to be over. Taking an extra two weeks to verify your damages fully documented and get a second repair estimate can put hundreds, sometimes thousands, more dollars in your pocket.

Maintaining a claim communication log is not bureaucratic overhead. According to best practices in claims documentation, organized files with bundled evidence lead to faster evaluation and fewer rework requests from adjusters. Every call, email thread, and document you submit should be logged with a date and a one-line summary.

When disputes escalate beyond informal conversation, you have options. You can request a supervisory review within the insurer’s claims department, file a complaint with your state’s Department of Insurance, or consult an attorney. If you believe your claim has been unfairly denied or lowballed, understanding why attorneys fight insurance companies in Colorado can clarify what legal intervention actually looks like and when it makes sense.

Understanding timelines in the claim resolution workflow

One of the most common frustrations with insurance claims is not knowing how long anything is supposed to take. Realistic expectations help you know when to follow up and when to escalate.

How long each stage typically takes

| Claim Stage | Typical Timeframe | Notes |

|---|---|---|

| Claim acknowledgment | 1 to 15 days | Varies by state; many states require 10 to 15 days |

| Investigation and review | 15 to 45 days | Longer for complex or disputed claims |

| Claim decision | 15 to 60 days from filing | State law governs maximum timelines |

| Payment after acceptance | 5 to 30 days | Depends on state regulations |

Insurers generally have 15 to 60 days to acknowledge and decide on a claim, followed by an additional 5 to 30 days to issue payment, though these windows vary significantly by state and claim type. California, Texas, and New York each have specific statutory deadlines that your insurer is legally required to meet.

What affects your timeline

Complexity is the biggest variable. A straightforward auto claim with no liability dispute and complete documentation can move from FNOL to payment in under three weeks. A personal injury claim involving ongoing medical treatment, disputed liability, or multiple parties can take months to years.

Insurance claim tracking matters during the investigation phase especially. Do not wait passively. Set a calendar reminder for every 10 to 14 days to follow up if you have not received an update. When you follow up, ask specifically: “What is the current status?” and “What is needed to move this forward?” Those two questions, asked in writing, create a paper trail and often prompt faster responses.

Legal protections exist for claimants when insurers fail to meet mandated timelines. Most states have bad faith insurance statutes that allow claimants to seek additional damages when an insurer unreasonably delays or denies a valid claim. Knowing those protections exist matters. You are not at the insurer’s mercy. The law sets boundaries on how long they can take your money and withhold a fair resolution.

What I have learned from a decade on both sides of claims

I spent years as a claims adjudicator for the federal government before I became a personal injury attorney in Colorado. That means I have reviewed claims from the inside and fought for claimants from the outside. What I have seen clearly in both roles is this: documentation is the single variable that separates fast, successful claims from slow, contested ones.

Most people treat documentation as an afterthought. They think the facts of the incident will speak for themselves. They do not. An adjuster reviewing your file is looking at dozens of files simultaneously. The claimant who hands them a structured, complete package gets resolved first. The claimant who provides fragments gets put on hold.

I have also learned that the tone of communication matters more than people realize. Adjusters are not your adversaries, but they are not your advocates either. They work for the insurer. Polite, organized, and persistent is the right posture. Aggressive or passive works against you. Think of it the way a mule approaches difficult terrain: steady, sure-footed, not easily thrown off course.

Where I see people get genuinely hurt is when they settle too quickly on injury claims. If your medical treatment is not complete, you do not know your full damages yet. Settling before you reach maximum medical improvement can leave significant money on the table for future care you did not anticipate. That is the moment when getting legal advice is not optional. It is necessary. A free consultation costs you nothing and could reframe your understanding of what you are actually owed.

— Ryan

When your claim needs more than a workflow

Understanding the process is a strong start. But when you are dealing with an accident that caused real injury, property loss, or a denial you believe is wrong, having the right legal support changes the outcome. Stubbornattorney has spent years fighting for injured Coloradans, and as a firm led by a former claims adjudicator, we know exactly how insurers evaluate files and where they push back. If you are unsure whether your settlement offer is fair, or if your claim has been delayed or denied, a free case review with our team gives you a clear picture with zero obligation. See common personal injury case examples that mirror what many of our clients faced, or go directly to our Colorado Springs personal injury page to request your free consultation today.

FAQ

What is the first step in an insurance claim workflow?

The first step is filing the first notice of loss (FNOL) with your insurer as soon as possible after the incident. A complete FNOL with photos, a timeline, and supporting documentation speeds up adjuster assignment and reduces delays.

How long does an insurance company have to resolve a claim?

Insurers generally have 15 to 60 days to decide on a claim and an additional 5 to 30 days to issue payment, depending on your state and claim type. State bad faith statutes can apply if an insurer misses these deadlines without valid reason.

What documents do I need to file an insurance claim?

You typically need photos of the damage, a police or incident report, contact and insurance information for all parties, receipts for related expenses, and any estimates for repair or replacement. Home claims also require a proof of loss form with an itemized inventory.

What should I do if my claim is taking too long?

Follow up every 10 to 14 days with a written request for a status update. Ask specifically what is needed to move the claim forward. If your insurer is missing statutory deadlines, you can file a complaint with your state’s Department of Insurance or consult a personal injury attorney.

When should I get an attorney for my insurance claim?

Get legal advice before settling any claim that involves injury, significant property loss, or a dispute over liability. If your medical treatment is not complete or your claim has been denied without a clear explanation, consulting an attorney costs nothing upfront and protects your right to full compensation. You can learn more about how injury documentation affects your claim value before making that decision.