What Is Financial Recovery After an Accident?

TL;DR:

- Financial recovery after an accident involves restoring your financial position to pre-accident levels through thorough documentation, legal action, and strategic negotiations. It encompasses medical expenses, lost wages, property damage, and non-economic damages like pain and suffering, often requiring careful management of insurance claims and legal avenues. Early legal advice and meticulous record-keeping significantly influence the total amount recovered and the quality of your financial rebuilding process.

Most people assume that financial recovery after an accident means filing a claim, getting a check, and moving on. The reality is far more layered. What is financial recovery after accident, really? It’s the process of restoring your financial position to where it was before the crash, covering everything from medical bills and lost wages to property damage and long-term care costs. This guide walks you through every stage of that process, from understanding what you’re owed to avoiding the mistakes that cost accident victims thousands of dollars every year.

Table of Contents

- Key takeaways

- What financial recovery after accident actually means

- Common financial challenges after a car accident

- Insurance claims: maximizing what you recover

- Legal avenues for financial compensation after accident

- Post-settlement financial planning and rebuilding

- My take on what most people get wrong about financial recovery

- How Stubbornattorney can help you recover what you’re owed

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Financial recovery means restoration | The goal is to return your finances to their pre-accident state, not just cover immediate bills. |

| Insurance rarely covers everything | Gaps in coverage for medical costs, lost income, and future care are common and significant. |

| Documentation protects your claim | Consistent medical records and organized expense tracking directly determine how much you recover. |

| Settlements come with deductions | Medical liens and other obligations reduce your actual take-home amount before you receive payment. |

| Early legal advice pays off | Involving an attorney early helps counter lowball offers and maximizes your net compensation. |

What financial recovery after accident actually means

Financial recovery after an accident means restoring your financial position to where it was before the crash occurred. That sounds simple. In practice, it requires identifying every loss you’ve suffered, quantifying it accurately, and then pursuing the right combination of insurance and legal remedies to get it covered.

The costs involved go much further than most people expect. Here is what a complete financial recovery typically includes:

- Medical expenses: Emergency room visits, surgeries, imaging, physical therapy, prescription medications, and future treatment related to your injuries

- Lost wages: Income you missed while recovering, plus reduced earning capacity if your injuries affect your ability to work long-term

- Vehicle and property damage: Repair or replacement costs for your car and any personal property inside it

- Out-of-pocket costs: Rental car fees, transportation to medical appointments, childcare you needed because of your injuries, and household help you had to hire

- Non-economic damages: Pain and suffering, emotional distress, loss of enjoyment of life, and loss of consortium

That last category is where many people underestimate what they’re owed. Non-economic damages are real losses. They are not bonuses. Courts and insurance carriers account for them separately from economic damages because the physical and emotional toll of a serious accident carries genuine value.

Lost wages, ongoing medical costs, increased insurance premiums, and credit damage are among the most common financial consequences victims face. Understanding that all of these categories exist, and that each one requires its own documentation strategy, is the foundation of any serious financial recovery effort.

Common financial challenges after a car accident

The weeks and months after a crash can feel like a financial avalanche. Even when you know help is available, the pressure of mounting bills while you’re physically unable to work is overwhelming.

The most immediate problem for many people is lost income. If you’re paid hourly or run your own business, missing two weeks of work has an immediate and painful impact on your household. If your injuries keep you out for months, the damage compounds. Your bills do not pause while your body heals.

Medical expenses create a second wave of pressure. Health insurance often covers only part of the costs, and many accident victims are uninsured or underinsured. Co-pays, deductibles, specialist fees, and treatments not deemed medically necessary by your carrier can add up to tens of thousands of dollars quickly.

Then comes a problem most people don’t anticipate: your auto insurance premiums may rise even if the accident was not your fault. At the same time, missed bill payments during recovery can damage your credit score, which creates downstream financial consequences that linger for years after you’ve physically healed.

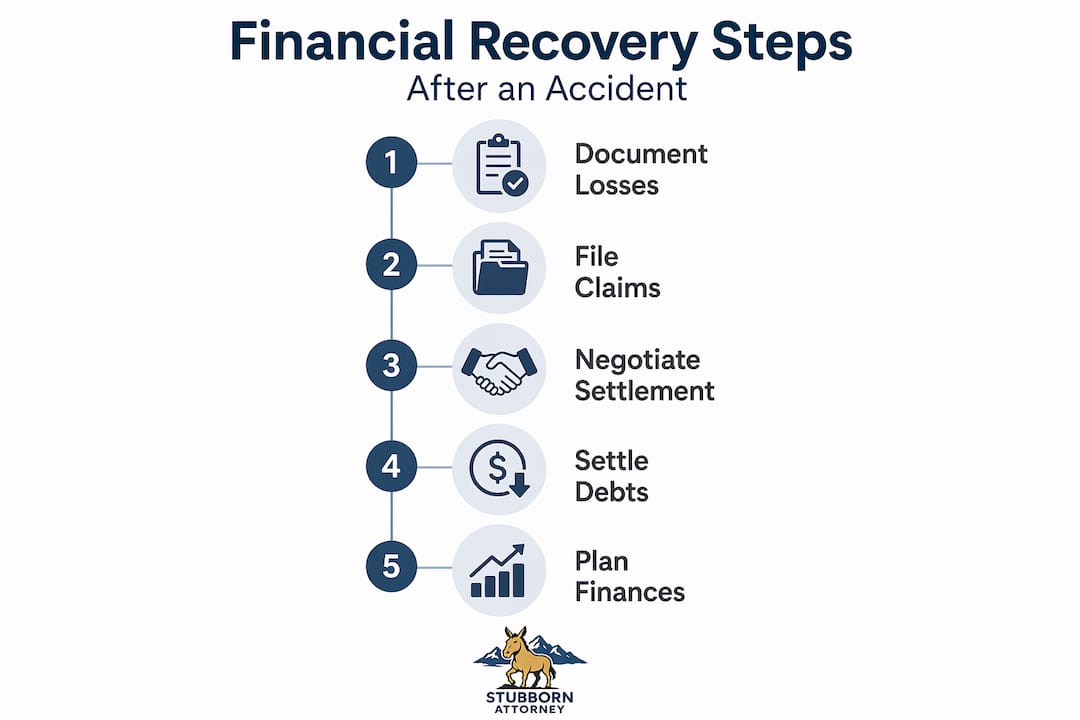

Here is a practical sequence for managing bills and expenses during recovery:

- Contact your creditors immediately. Many lenders, utility companies, and medical providers offer hardship programs or payment deferrals. You have to ask. Most of them will not proactively offer these options.

- Identify emergency assistance programs. State and county programs exist specifically for individuals in financial crisis. Nonprofit organizations, hospital charity care programs, and community assistance funds can help cover gaps.

- Track every expense related to the accident. Every receipt, every mileage log, every co-pay. These records form the backbone of your compensation claim.

- Prioritize essential bills. Rent, utilities, and food come first. Unsecured debt like credit cards can often be managed last without the same immediate consequences.

- Do not accept early settlement offers out of desperation. This is where financial pressure becomes a legal trap, and where many victims lose the most money.

Pro Tip: If you cannot afford your medical treatment while your claim is pending, ask your attorney about medical liens. Some providers will treat you now and wait to be paid from your settlement, which removes the immediate financial pressure without requiring you to pay out of pocket.

Insurance claims: maximizing what you recover

Understanding how auto insurance works after an accident is the single most practical thing you can do before you ever file a claim. The system is not designed to pay you fully and automatically. It’s designed to pay what it must.

The main types of coverage that come into play after a crash include Personal Injury Protection (PIP), which pays for your medical bills and lost wages regardless of fault; liability coverage, which covers your damages if someone else caused the crash; MedPay, which supplements medical cost coverage; and uninsured/underinsured motorist coverage, which protects you when the at-fault driver has insufficient insurance.

Treatment within 14 days is required in Florida for PIP benefits, and similar deadlines exist in other states. Missing these windows does not just cost you a benefit. It signals to the insurer that your injuries may not be serious, which affects the value of your entire claim.

Gaps in medical treatment records may lead insurers to reduce or deny compensation claims by questioning injury severity or causation. Consistent documentation is your evidentiary foundation. That means attending every appointment, following your doctor’s treatment plan, and keeping records of everything.

Here’s what adjusters actually look for when they evaluate your claim:

- The severity and consistency of your documented injuries

- Whether your treatment aligns with what your diagnosis would typically require

- Any gaps between the accident date and your first medical visit

- Recorded statements you’ve made that could be used to minimize your injuries

- Photos, police reports, and witness statements that establish fault

Insurance companies use quick, lowball offers to encourage rapid claimant acceptance before victims fully understand the scope of their damages. An offer that seems generous on day five may be deeply inadequate once you understand your full treatment timeline.

Pro Tip: Never give a recorded statement to the opposing insurance company without first speaking to an attorney. Adjusters are trained to ask questions in ways that minimize your injuries. Anything you say can and will be used to reduce your payout.

Knowing when to hire an automobile accident attorney can be the difference between a fair settlement and one that leaves you covering thousands of dollars in costs yourself. In general, if your injuries required any medical treatment, involve lost wages, or are anything beyond minor, legal representation is worth considering immediately.

Legal avenues for financial compensation after accident

When insurance payouts fall short, which happens more often than not in serious crashes, a personal injury claim is your path to full financial compensation after accident. Filing a lawsuit or negotiating a settlement through an attorney gives you access to damages that insurance alone will never cover.

A personal injury claim allows you to pursue compensation for future medical expenses, lost earning capacity, pain and suffering, emotional distress, and punitive damages in cases involving gross negligence. These categories are largely inaccessible through a standard insurance claim. Legal representation helps maximize compensation by ensuring these future and non-economic costs are accounted for from the start.

Most personal injury cases settle before going to trial. Here is a direct comparison of the two main resolution options:

| Settlement type | Pros | Cons |

|---|---|---|

| Lump-sum settlement | Immediate access to funds; no ongoing legal exposure | Must manage the full amount responsibly; taxes on certain portions may apply |

| Structured settlement | Provides long-term income stream; reduces risk of overspending | Less flexibility; difficult to renegotiate terms later |

| Trial verdict | Potential for higher award including punitive damages | Lengthy process; unpredictable outcome; higher legal costs |

One detail that surprises many accident victims: settlement proceeds often must cover medical liens, subrogation claims, and other case expenses before you receive your net compensation. Your health insurer, for example, may have a right to be reimbursed from your settlement for the bills they paid on your behalf. Your attorney’s fees come out as well. The gross settlement number is almost never what you take home.

This is why understanding accident financial recovery requires looking at the full picture, not just the headline settlement amount. A skilled attorney negotiates those liens down, which directly increases your net recovery. That negotiation process alone can be worth thousands of dollars.

Legal strategies post-accident often prioritize gathering meticulous documentation to counter insurer tactics that seek to devalue claims through alleged inconsistencies or gaps in evidence. The stronger your records, the stronger your negotiating position, and the less likely an insurer is to fight you.

Post-settlement financial planning and rebuilding

Receiving a settlement check is not the finish line. It’s the starting point for a new set of financial decisions, and the choices you make in the months after settlement can either protect your future or create new problems.

The most important concept to internalize is that settlement money is replacement money. It is meant to cover losses you have already suffered and losses you will continue to suffer going forward. Treating it like a windfall leads to decisions that leave accident victims in financial distress years later.

Here is what smart post-settlement financial planning looks like:

- Account for ongoing medical costs first. If your injuries require future surgeries, therapy, or medication, set aside those funds before anything else. Running out of money for necessary treatment is the worst outcome.

- Pay down high-interest debt. Debt accumulated during recovery, especially credit card balances, grows quickly. Eliminating it reduces monthly financial pressure.

- Build an emergency fund. Three to six months of living expenses in a liquid account protects you from the next financial disruption without requiring you to go into debt.

- Consult a fee-only financial advisor. Consulting fee-only financial advisors and creating long-term plans protects your compensation money from being depleted too quickly.

- Understand the tax implications. Personal injury settlements for physical injuries are mostly non-taxable, but punitive damages and interest on a settlement may be taxable. A tax professional can help you avoid surprises.

The most common mistake people make after settlement is addressing wants before needs. A new car, a vacation, or debt for a family member feels urgent. Your long-term medical and living stability are more urgent. Protect those first.

My take on what most people get wrong about financial recovery

I’ve represented injured clients in Colorado for over a decade, and before that, I worked as a claims adjudicator for the federal government. I’ve sat on both sides of this process. What I’ve learned is that most accident victims underestimate how much of this fight is decided in the first few weeks.

The single biggest mistake I see is waiting too long to get legal advice. People assume an attorney only matters when you’re filing a lawsuit. That’s wrong. The decisions you make in the first 30 days, what you say to adjusters, whether you go to the doctor consistently, what records you keep, set the ceiling for your entire claim. By the time someone walks into my office frustrated with a lowball offer, some of the damage is already done.

The second thing I’ve learned is that the hidden costs are often larger than the obvious ones. Medical bills are visible. Lost earning capacity, future care needs, and the emotional toll of a serious injury are not. Many clients don’t even think to raise these issues because they feel speculative. They’re not. Courts recognize them, and so do skilled negotiators.

I also want to be direct about rushing settlements. I understand the financial pressure. When you can’t pay your rent and an insurance company is offering you money, taking it feels like relief. But in my experience, every client who accepted an early offer before understanding the full scope of their injuries regretted it. The pressure is real, but it’s also temporary. The consequences of a bad settlement are permanent.

What gives me the most satisfaction is clients who come in overwhelmed and leave with a clear plan. That’s what understanding accident financial recovery should do for you. Not fear, not paralysis. A clear picture of what you’re owed, and a path to getting it.

— Ryan

How Stubbornattorney can help you recover what you’re owed

At Stubbornattorney, we don’t take every case. We take your case and refuse to let go. Ryan Malnar has spent over a decade fighting for injured Coloradans, and his background as a former federal claims adjudicator means he knows exactly how insurers think and how to counter them. That’s not a claim we make lightly. It’s the reason we’ve recovered millions of dollars in settlements for people who were told their cases weren’t worth much.

Whether you’re dealing with a disputed liability claim, a lowball settlement offer, or a complex injury with long-term consequences, the right time to talk to us is now. Waiting costs you options. You can review common personal injury case examples to see how cases like yours have been handled, or go directly to our Colorado Springs personal injury services page to start your free case review. If you’re in the Burlington area, our Burlington injury team is ready to help. There is no cost to talk. There is a real cost to waiting.

FAQ

What does financial recovery after an accident include?

Financial recovery after an accident covers all losses caused by the crash, including medical bills, lost wages, property damage, out-of-pocket expenses, and non-economic damages like pain and suffering. The goal is to restore your financial position to where it was before the accident occurred.

How long does financial recovery after a car accident take?

The timeline varies widely depending on the severity of your injuries, the complexity of the insurance claims process, and whether a personal injury lawsuit is filed. Minor claims may resolve in a few months, while serious injury cases can take one to three years to reach a full settlement.

Can I recover costs after an accident if the other driver was uninsured?

Yes. Uninsured motorist coverage on your own policy can cover your medical expenses and other damages when the at-fault driver has no insurance. A personal injury attorney can also explore other avenues for recovery depending on the circumstances.

What should I expect after an accident when dealing with insurance companies?

Expect the insurance adjuster to evaluate your claim with the goal of minimizing what they pay out. Early settlement offers are often lower than your full damages. Consistent medical documentation, organized records, and legal guidance significantly improve your outcome.

How does hiring an attorney affect my financial compensation after accident?

An attorney can identify damages you may have overlooked, negotiate medical liens to increase your net recovery, and push back against lowball offers that insurers rely on when victims represent themselves. Most personal injury attorneys work on contingency, meaning you pay nothing unless you win.