Gap Insurance After an Accident: What You Need to Know

Gap insurance is supplemental auto coverage that pays the difference between your vehicle’s actual cash value and the remaining balance on your loan or lease after a total loss. The industry term is Guaranteed Asset Protection, commonly shortened to GAP. If you’ve just been in an accident and your car is totaled, understanding what is gap insurance after accident situations is the difference between walking away clean and owing thousands of dollars on a car you no longer have. According to NerdWallet, your primary insurer pays the actual cash value minus your deductible first, and gap insurance covers whatever loan balance remains after that payout. Amica Insurance confirms that gap coverage supplements, but does not replace, your collision and comprehensive policies.

What is gap insurance after an accident?

Gap insurance activates after your vehicle is declared a total loss and your primary insurer has finalized its payout. The sequence matters. Your collision or comprehensive coverage pays first, and only then does the gap calculation begin.

Here is the core mechanic: your car depreciates the moment you drive it off the lot. A vehicle worth $30,000 at purchase can drop to $22,000 in actual cash value within two years. If your loan balance is still $27,000 when the accident happens, your primary insurer pays $22,000 minus your deductible. That leaves a $5,000-plus gap you would owe the lender out of pocket. Gap insurance covers that shortfall.

The gap payout goes directly to your lender, not to you. You do not receive a check to spend elsewhere. The sole purpose of the payment is to zero out or reduce the remaining loan or lease balance after the primary settlement.

Gap coverage also applies to unrecovered theft, not just accidents. If your car is stolen and never found, the same mechanics apply: primary insurer pays ACV, gap covers the remaining balance.

Pro Tip: Before you assume gap insurance will cover everything, pull your loan payoff statement and compare it to your insurer’s ACV estimate. That single comparison tells you exactly how much gap coverage you need and whether you are actually “upside down” on your loan.

What does gap insurance cover vs. what it excludes?

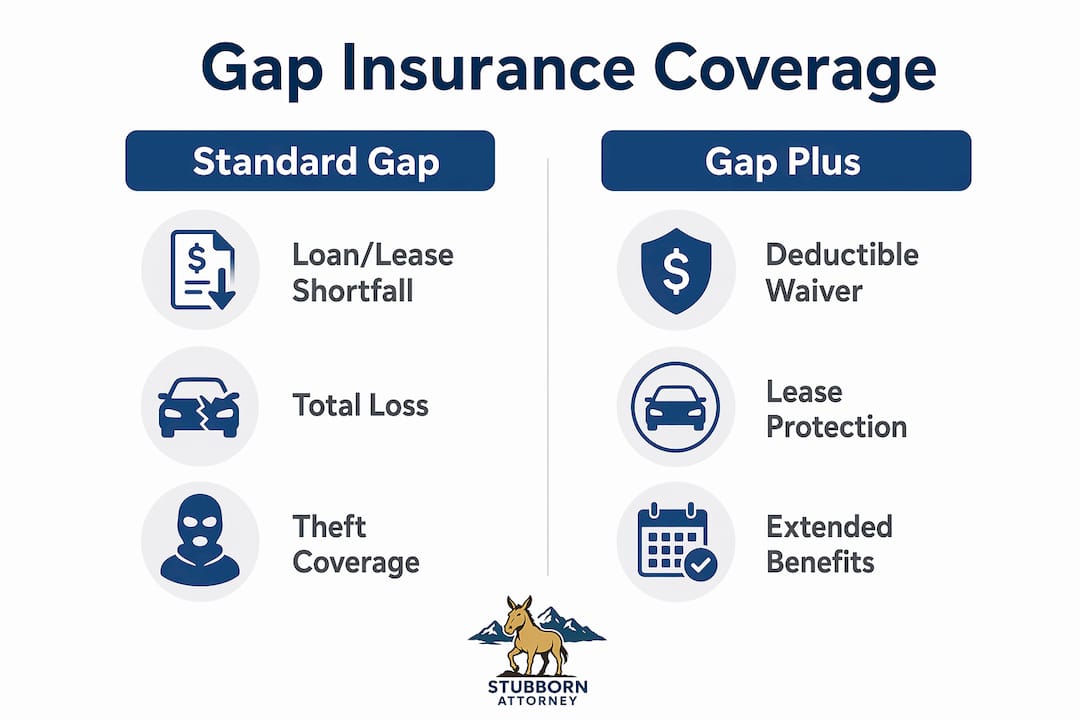

Gap insurance covers one thing precisely: the difference between your insurer’s ACV settlement and your remaining loan or lease payoff. Nothing more, nothing less.

The table below clarifies what is and is not included under a standard gap policy:

| Coverage Item | Standard Gap Insurance | Gap Plus / Deductible Waiver |

|---|---|---|

| Loan/lease balance shortfall | Yes | Yes |

| Collision/comprehensive deductible | No | Yes (if explicitly stated) |

| Vehicle repairs | No | No |

| Medical expenses | No | No |

| Replacement vehicle costs | No | No |

| Negative equity rolled from prior loan | Sometimes excluded | Sometimes excluded |

Gap insurance does not pay for your deductible unless your policy explicitly includes a deductible waiver or “gap plus” provision. Most standard contracts exclude this, and many car owners discover that fact only after filing a claim.

Gap coverage also stays dormant until the total loss status is confirmed and the primary insurer’s payout is finalized. You cannot file a gap claim while your car is still being assessed for repairs. The gap claim remains inactive until both conditions are met.

The difference between gap and full coverage is also worth clarifying. Full coverage refers to carrying both collision and comprehensive insurance. Gap is a separate add-on layer. Collision and comprehensive coverage are actually prerequisites for gap insurance to apply. If you do not have them, gap will not pay out regardless of what your contract says.

Pro Tip: Read your gap contract before an accident, not after. Look specifically for the words “deductible waiver” or “gap plus.” If those phrases are absent, plan to pay your deductible out of pocket even when gap activates.

Who benefits most from gap insurance after a total loss?

Gap insurance delivers the clearest financial benefit when your loan balance exceeds your vehicle’s actual cash value at the time of the accident. Several specific situations create that condition.

- New car buyers with low down payments. A down payment under 20% means you start the loan already close to or below the vehicle’s depreciating value. Gap coverage benefits first-time buyers and lessees who put less than 20% down precisely because depreciation outpaces early loan payments.

- Lessees. Lease agreements often require gap coverage because the leasing company carries the financial risk of a total loss gap.

- Buyers of fast-depreciating vehicles. Some makes and models lose value faster than average. If your vehicle depreciates quickly, the gap between ACV and loan balance stays wide longer.

- Buyers who rolled negative equity from a prior loan. If you owed more on your trade-in than it was worth and rolled that balance into a new loan, you started the new loan already upside down.

- Long-term loan holders. 72-month and 84-month auto loans have become common. The longer the term, the slower the principal drops, and the longer you remain exposed to a gap.

The crucial post-accident question is always the same: what is your insurer’s ACV settlement, and what is your loan payoff balance? If the payoff exceeds the ACV, gap insurance is not just useful. It is the only thing standing between you and a four-figure or five-figure out-of-pocket bill on a car you can no longer drive.

Gap coverage also provides peace of mind during the months when depreciation is steepest, typically the first two to three years of ownership. After that window, most borrowers have paid down enough principal that the loan balance falls below or near the vehicle’s value, and gap becomes less necessary.

How much does gap insurance cost?

Gap insurance purchased through an auto insurer costs $50 to $150 per year. Dealership or lender products run significantly higher, typically $500 to $700 total, and that amount is often financed into the loan with interest added on top.

| Purchase Source | Typical Cost | Financing Risk | Flexibility |

|---|---|---|---|

| Auto insurer (add-on) | $50–$150/year | None | Cancel anytime |

| Dealership / lender | $500–$700 total | Often financed with interest | Locked into loan term |

| Credit union | Varies, often competitive | Sometimes financed | Moderate |

The cost difference between insurer and dealership gap is not trivial. A $600 dealership gap product financed at 7% over 72 months costs you more than $750 in total. The same protection through your auto insurer costs $300 or less over the same period.

Gap coverage through an insurer also requires that you already carry collision and comprehensive coverage on the same vehicle. You cannot add gap to a liability-only policy. That prerequisite exists because gap is a secondary layer. Without primary coverage, there is no ACV payout for gap to supplement.

One more condition applies: gap insurance is only available while you still owe money on the vehicle. Once your loan is paid off, gap has no purpose and most policies cancel automatically or allow you to cancel for a prorated refund.

Reviewing contract terms after purchasing gap through a dealership is critical. Dealer gap products sometimes include caps on the maximum payout, exclusions for negative equity rolled from prior loans, and different deductible terms than insurer-issued policies.

How to file a gap insurance claim after a total loss accident

Filing a gap claim follows a specific sequence. Skipping steps or filing out of order delays your payout and can create complications with your lender.

-

File your primary auto insurance claim immediately. Contact your collision or comprehensive insurer and report the accident. Request that the vehicle be evaluated for total loss status. Do not wait. The gap claim process cannot begin until the primary claim is resolved.

-

Obtain the total loss declaration and ACV settlement details. Your primary insurer will issue a written determination that the vehicle is a total loss and state the ACV payout amount after your deductible. Keep this document. It is the foundation of your gap calculation.

-

Request a loan payoff statement from your lender. Contact your bank, credit union, or finance company and ask for the current payoff balance as of the date of the accident. This figure must match the date of loss, not the current date, since interest accrues daily.

-

Gather all required documentation. A standard gap claim requires the police report if the loss involved theft or a criminal incident, the finalized insurer settlement letter, the loan payoff statement, and your gap policy number. The gap claim documentation must come from both your insurer and your lender.

-

Submit your gap claim to the gap insurer or provider. If you purchased gap through your auto insurer, file through the same company. If you purchased through a dealership or lender, contact that provider directly. Submit all documents together to avoid back-and-forth delays.

-

Coordinate the payout with your lender. The gap payout amount is calculated based on the ACV after deductible, not the original purchase price. The check goes directly to the lender. Confirm with your lender that the payment has been received and applied to your account.

Timing matters throughout this process. Some gap policies require you to file within a set number of days after the primary claim is settled. Check your contract for that deadline and treat it as firm. Missing it can void your claim entirely.

For a broader look at the insurance claim workflow, Stubbornattorney has a step-by-step guide that covers the full process from accident report to final settlement.

What i’ve learned about gap insurance claims from the other side

I spent years as a claims adjudicator for the federal government before I became a personal injury attorney. I have seen gap insurance from both sides of the table, and the pattern I see most often is this: car owners assume gap insurance is a safety net that catches everything. It does not.

The most common shock I see is the deductible. A client totals their car, the primary insurer pays ACV minus a $1,000 deductible, and the gap policy covers the loan shortfall. But that $1,000 deductible is still out of pocket. Nobody told them that at the dealership when they signed the gap addendum. The deductible exclusion is buried in the contract, and most buyers never read it.

The second thing I see is clients who accept the insurer’s ACV figure without questioning it. ACV is not a fixed number. Insurers calculate it using their own tools and databases, and those figures are not always accurate. You have the right to dispute an ACV determination. If the insurer undervalues your vehicle, your gap amount increases, and you may end up owing more than you should. Always compare the ACV offer against independent sources like Kelley Blue Book or NADA Guides before accepting.

My honest advice: buy gap through your auto insurer, not the dealership. The cost difference is real, the terms are usually cleaner, and you can cancel it the moment your loan balance drops below your vehicle’s value. Dealer gap products are often financed into the loan, which means you pay interest on your insurance. That is a bad deal by any measure.

If you are already past the accident and dealing with a gap claim dispute or an ACV settlement that feels wrong, do not handle it alone. Understanding how to claim and win after an auto accident requires knowing exactly how insurers evaluate your vehicle and your claim. That knowledge is the difference between a fair settlement and leaving money on the table.

— Ryan

When a gap insurance dispute needs legal support

Gap insurance disputes and low ACV settlements are more common than most car owners realize. When your insurer undervalues your vehicle or your gap provider denies a claim, the financial exposure can reach thousands of dollars. Stubbornattorney represents injured Colorado drivers who are fighting exactly these battles.

Ryan Malnar and the team at Stubbornattorney have recovered millions of dollars for accident victims across Colorado Springs, Pueblo, and beyond. If your gap claim has been delayed, denied, or underpaid, or if your primary insurer’s ACV settlement seems far below your vehicle’s actual value, a free case review can clarify your options fast. You should not be paying out of pocket because an insurer got the numbers wrong.

FAQ

What is gap insurance after an accident?

Gap insurance is supplemental coverage that pays the difference between your vehicle’s actual cash value and your remaining loan or lease balance after a total loss. It activates only after your primary insurer has finalized the ACV payout and declared the vehicle a total loss.

Does gap insurance cover my deductible?

Standard gap insurance does not cover your collision or comprehensive deductible. Your deductible remains out of pocket unless your policy explicitly includes a deductible waiver or “gap plus” provision.

How long does a gap insurance payout take?

Gap payouts depend on the primary insurer completing its total loss determination first. Once you submit all required documents, including the settlement letter and loan payoff statement, most gap providers process the claim within a few weeks.

Is gap insurance worth it for a new car?

Gap insurance is worth it when your loan balance exceeds your vehicle’s actual cash value, which is most common in the first two to three years of ownership, especially with low down payments or long loan terms.

Can i get gap insurance after an accident has already happened?

Gap insurance cannot be added after an accident has already occurred. Coverage must be in place before the loss event. If you did not have gap coverage at the time of the accident, you are responsible for any difference between the ACV payout and your loan balance.