Why Insurance Denies Claims: What You Need to Know

Insurance claim denial is defined as an insurer’s formal refusal to pay a submitted claim, citing policy exclusions, procedural errors, or unmet conditions. Understanding why insurance denies claims is the first step toward fighting back effectively. U.S. home insurers denied 12.3% of first-party claims in 2023, with water damage denials reaching 18.4% and named storm denials hitting 14.9%. Those numbers represent real people left without the coverage they paid for. Most denials fall into three categories: contractual coverage issues, administrative errors, and investigation disputes. Each category has a different fix, and knowing which one you are dealing with changes everything.

Why insurance denies claims: policy clauses most people never read

The most common contractual reason for claim rejection is a policy exclusion the policyholder never knew existed. Insurance policies routinely run 40 or more pages, written in dense legal language that shifts compliance burdens onto consumers. A 2024 Insurance Research Council survey found that 72% of policyholders with denied claims had not read or recalled reading the specific clause cited in the denial. That figure explains why so many people are blindsided when a claim gets rejected.

Several specific clauses drive the majority of contractual denials:

- Named-storm deductibles. Many homeowner policies apply a separate, higher deductible when damage results from a named hurricane or tropical storm. Standard deductibles do not apply, and the difference can be tens of thousands of dollars.

- Anti-concurrent causation clauses. These clauses allow insurers to deny claims entirely when a covered peril and an excluded peril contribute to the same loss. Wind damage combined with flood damage is the classic example. Even if wind caused most of the destruction, the presence of excluded flood damage can void the entire claim.

- Sewer backup and mold exclusions. Standard homeowner policies typically exclude sewer backup and resulting mold damage unless the policyholder purchased a separate endorsement. Many do not realize this until water backs up into their basement.

- Vacancy clauses. Policies often exclude coverage if a property has been unoccupied for 30 or 60 consecutive days. A second home left empty over winter can lose coverage without the owner knowing.

- Maintenance exclusions. Damage attributed to gradual deterioration or lack of upkeep is almost universally excluded. Insurers use this clause broadly, sometimes applying it to damage that was sudden and accidental.

Pro Tip: Read your declarations page and the exclusions section of your policy before you ever need to file a claim. Pay specific attention to any clause that begins with “we do not cover” or “this policy excludes.”

Dense policy language is not accidental. It is a structural feature that places the burden of understanding complex legal terms on the consumer. Knowing the specific clause your insurer cited gives you a concrete target to challenge in an appeal.

How do technical and administrative errors lead to claim denials?

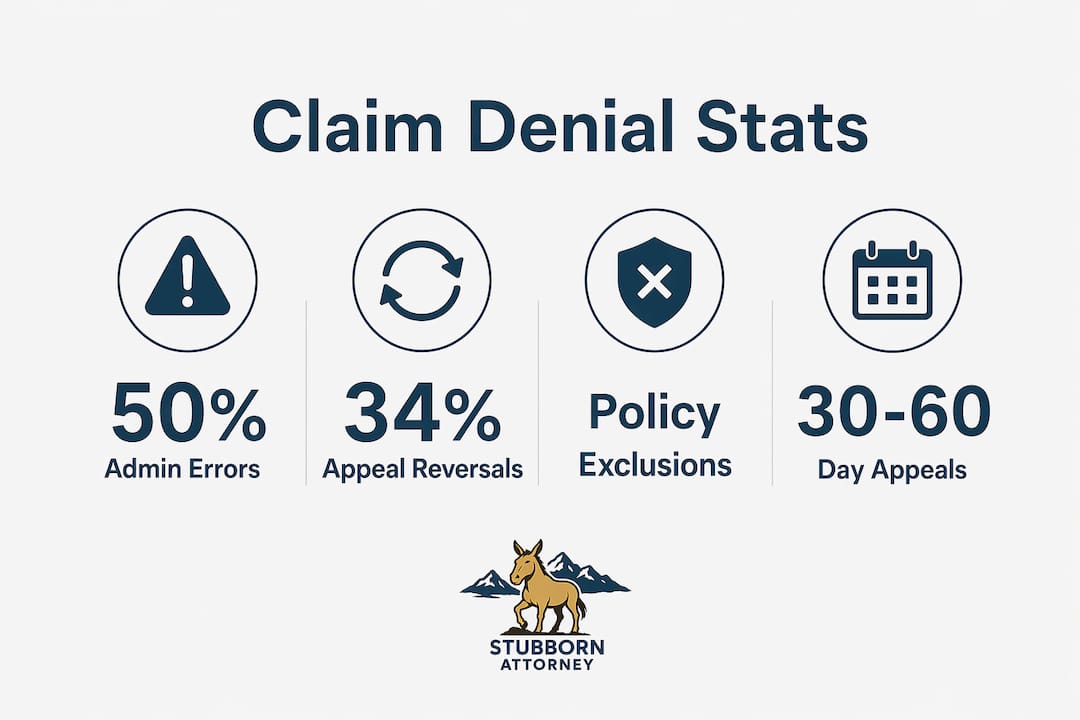

Administrative errors are the most fixable category of claim rejection, and they are far more common than most people realize. Up to 80% of denials stem from preventable intake or front-desk errors rather than genuine coverage disputes. That means the majority of denied claims were never actually reviewed on their merits.

The most frequent administrative errors include:

- Wrong or missing identification numbers. Incorrect policy numbers, member IDs, or provider codes trigger automatic rejections before a human ever reviews the file.

- Eligibility and registration errors. 40% of medical claim denials result from eligibility or registration mistakes, such as a lapsed policy date or an incorrect coverage period listed on the form.

- Missing or incomplete forms. A single missing attachment, unsigned authorization, or absent supporting document is enough to reject an otherwise valid claim.

- Duplicate claim submissions. Submitting the same claim twice, even accidentally, flags the second submission as a duplicate and results in automatic denial.

- Late filing. Every policy sets a deadline for reporting a loss and submitting a claim. Missing that window by even one day gives the insurer grounds to deny on procedural grounds alone.

The table below shows the most common administrative denial types and how quickly each can typically be resolved:

| Denial type | Common cause | Typical resolution time |

|---|---|---|

| Wrong ID or policy number | Data entry error | 1–5 business days |

| Eligibility error | Lapsed or incorrect coverage date | 3–10 business days |

| Missing documentation | Incomplete submission | 5–14 business days |

| Duplicate claim | Accidental resubmission | 1–3 business days |

| Late filing | Missed deadline | Requires appeal or waiver |

Missing or inaccurate claim data is cited by 50% of revenue cycle leaders as the top denial cause across industries. The good news is that most of these errors are correctable through resubmission or a simple appeal letter.

Pro Tip: Request your denial reason code in writing immediately after receiving a rejection. Reason codes identify the exact administrative error, which tells you precisely what to fix before resubmitting.

What coverage and investigation tactics do insurers use to deny claims?

Beyond policy clauses and paperwork, insurers use active investigation strategies to reduce or eliminate payouts. These tactics are legal, but they are also aggressive, and policyholders who do not understand them are at a serious disadvantage.

The most common investigation-based denial tactics include:

- Pre-existing damage allegations. Insurers routinely argue that damage existed before the covered event. Most policyholders lack pre-loss date-stamped photos, which allows insurers to shift the burden of proof onto the claimant without strong counter-evidence.

- Wear-and-tear exclusions applied broadly. A roof that is 15 years old and sustains hail damage may be partially or fully denied on the grounds that deterioration contributed to the loss. Insurers use this argument even when the storm clearly caused the damage.

- Anti-concurrent causation in complex losses. Legal experts warn that anti-concurrent causation clauses are a default denial tactic after major storms. When wind and flood damage occur together, insurers use this clause to deny the entire claim rather than separating covered from excluded damage.

- Notice and cooperation requirements. Policies require prompt notice of a loss and full cooperation during the investigation. Failing to report quickly, refusing an inspection, or not providing requested documents gives the insurer grounds to deny based on a breach of policy conditions.

- Partial denial on scope disputes. Insurers frequently accept that a loss occurred but dispute the extent of damage. They may approve repair of one room while denying the rest, or accept structural damage while rejecting interior contents.

“Insurers shift the burden of proof to claimants through requirements for pre-loss photos and documentation. Without that evidence, the policyholder is left arguing against an insurer’s expert with no counter-documentation of their own.”

The burden of proof in a claim dispute sits squarely on the policyholder. That reality makes pre-loss documentation one of the most powerful tools available before a claim is ever filed. Understanding insurance bad faith tactics is equally critical, because some investigation practices cross the line from aggressive into legally actionable conduct.

How can you effectively appeal a denied insurance claim?

A denial letter is not the end of the road. 34% of denied claims are fully or partially reversed on appeal or complaint filing. That reversal rate reflects the fact that many initial denials are based on cursory automated reviews, not thorough human analysis.

The steps below give you the best chance of reversing a denial:

- Request the full denial explanation in writing. The insurer must identify the specific policy language or procedural rule behind the denial. Vague explanations are not acceptable, and you have the right to demand specifics.

- File your internal appeal promptly. Most policies and state regulations set a deadline for internal appeals, often 30–60 days from the denial date. Missing this window can forfeit your right to challenge the decision.

- Gather targeted documentation. Match your evidence directly to the denial reason. If the insurer claims pre-existing damage, obtain contractor reports, date-stamped photos, and maintenance records. If the denial cites a policy exclusion, research whether that exclusion applies to your specific facts.

- Get an independent expert opinion. A licensed public adjuster or structural engineer can provide a written assessment that contradicts the insurer’s findings. Independent expert reports carry significant weight in appeals and litigation.

- File a complaint with your state insurance commissioner. State regulators have authority to investigate improper denials. A formal complaint creates a record and often prompts the insurer to reconsider.

- Consult a personal injury or insurance attorney. When the denial involves significant money or bad faith conduct, legal counsel changes the dynamic entirely. Attorneys who understand how to strengthen injury claims can identify procedural violations and build a case for reversal or litigation.

Pro Tip: Never accept a verbal denial. Get every communication in writing, including the denial letter, any requests for additional information, and all correspondence during the appeal. Written records are your most powerful asset.

The insurance claim workflow matters as much as the underlying facts of your loss. A well-documented, timely appeal filed through the correct channels dramatically improves your odds of a successful outcome.

What I have learned from a decade of fighting insurance denials

Having spent years as a former claims adjudicator for the federal government before becoming a personal injury attorney, I have seen the denial process from both sides of the table. The single most consistent pattern I observe is this: policyholders are shocked by denials that were entirely predictable based on the policy they signed.

The clause that denies your claim was in your policy on day one. Insurers count on the fact that most people will not read a 45-page document written in legal language. That is not cynicism. It is the structural reality of how insurance contracts are designed, and it is why I tell every client to read their exclusions section before they ever need to file.

Administrative denials are the quick wins I see most often. A wrong ID number, a missing form, a lapsed eligibility date. These get fixed in days when you know what to look for. The denial reason code tells you exactly what went wrong. Most people never request it.

What concerns me more are the investigation-based denials, where an insurer’s adjuster arrives with a conclusion already formed and builds a file to support it. Pre-existing damage allegations without any pre-loss baseline are a red flag. If an insurer cannot show you evidence that the damage existed before your covered event, that argument should not stand. But it does stand, repeatedly, because policyholders have no counter-documentation.

My advice is direct: photograph your property every year, keep maintenance records, and read your policy. If you receive a denial, do not accept it as final. Request the reason code, read the cited clause, and file your appeal within the deadline. If the denial involves a significant amount or feels like bad faith, talk to an attorney before you respond. The appeal window closes fast, and the decisions you make in the first 30 days after a denial determine most of what is possible afterward.

— Ryan

When a denied claim needs legal backup

A denied insurance claim does not have to be the final word, especially when the stakes involve a personal injury or significant property loss. Stubbornattorney has recovered millions of dollars in settlements for Colorado clients whose claims were initially rejected or undervalued. Ryan Malnar’s background as a former federal claims adjudicator means the firm understands exactly how insurers evaluate and deny claims, and how to counter those decisions effectively.

If your claim has been denied and you are not sure what to do next, a free personal injury case review is the right first step. Stubbornattorney takes only injured victim cases, which means every resource goes toward getting you the result you deserve. Review common personal injury case examples to see how similar situations have been resolved, and reach out to start your consultation today.

FAQ

Why do insurance companies deny claims most often?

The most common claim denial reasons are policy exclusions, administrative errors such as missing or incorrect information, and late filing. 72% of denied policyholders were unaware of the specific clause cited in their denial.

Can a denied insurance claim be reversed?

Yes. 34% of denied claims are fully or partially reversed through an internal appeal or state complaint filing. Filing promptly with targeted documentation significantly improves the outcome.

What is an anti-concurrent causation clause?

An anti-concurrent causation clause allows an insurer to deny the entire claim when a covered peril and an excluded peril both contribute to a loss, even if the covered peril caused most of the damage.

How long do I have to appeal a denied claim?

Appeal deadlines vary by policy and state law, but most internal appeal windows run 30–60 days from the denial date. Missing this deadline can eliminate your right to challenge the decision.

When should I hire an attorney for a denied claim?

Hire an attorney when the denial involves a large dollar amount, a bad faith investigation, or a complex policy clause dispute. Legal counsel is especially valuable when the insurer has shifted the burden of proof onto you without sufficient evidence to support their position.