What Is a Lien in Injury Cases: Your Settlement Guide

If you’ve recently settled a personal injury claim, you may have been surprised to learn the check you receive is smaller than the number your attorney announced. That’s often because of liens. Understanding what is a lien in injury cases is one of the most practical things you can do to protect your financial recovery. A lien is a legal claim placed on your settlement proceeds by a third party who paid for something on your behalf, typically your medical care. Before you see a dollar, those claims must be addressed. This guide breaks down how liens work, who places them, and what you can do to minimize their impact.

Table of Contents

- What is a lien in injury cases

- Types of liens you will encounter

- How liens affect your settlement payout

- Legal obligations in lien resolution

- Practical tips for managing liens in your case

- My experience with liens and what most people get wrong

- How Stubbornattorney fights for your full recovery

- FAQ

What is a lien in injury cases

At its core, a lien is a legal right one party holds over another party’s money or property as security for a debt. In personal injury cases, that debt is almost always medical treatment you received after your accident. When a hospital, insurer, or government program pays your medical bills while your case is pending, they aren’t doing it out of charity. They’re doing it with the legal expectation of being repaid from your eventual settlement.

The lien definition in injury claims is more specific than the general legal concept. Here, a lien attaches directly to your settlement proceeds, not to your home or your bank account. The lienholder has no claim against your personal assets. Their claim lives inside the settlement fund itself, which means those funds cannot be fully released to you until the lien is resolved.

Who can place a lien on your settlement? The list is broader than most people expect:

- Medical providers: Hospitals, physicians, surgeons, physical therapists, and chiropractors can all assert liens for unpaid treatment tied to your injury.

- Health insurers: If your private health insurance paid your injury-related bills, your policy likely includes a subrogation clause, giving the insurer the right to recover those payments from your settlement.

- Medicare and Medicaid: These federal and state programs have statutory lien rights that go beyond what private insurers can claim.

- Workers’ compensation carriers: If you received workers’ comp benefits for the same injury, the carrier typically has a lien on your third-party settlement.

- Your own attorney: Attorney liens secure unpaid legal fees and costs advanced on your behalf.

The legal basis for most liens traces to contractual agreements (like your insurance policy), state statutes (like hospital lien laws), or federal law. The purpose is straightforward: to prevent you from being “made whole twice” by collecting full compensation while leaving the entities that funded your care unpaid. Whether that’s always fair is another question, and it’s one worth exploring.

Types of liens you will encounter

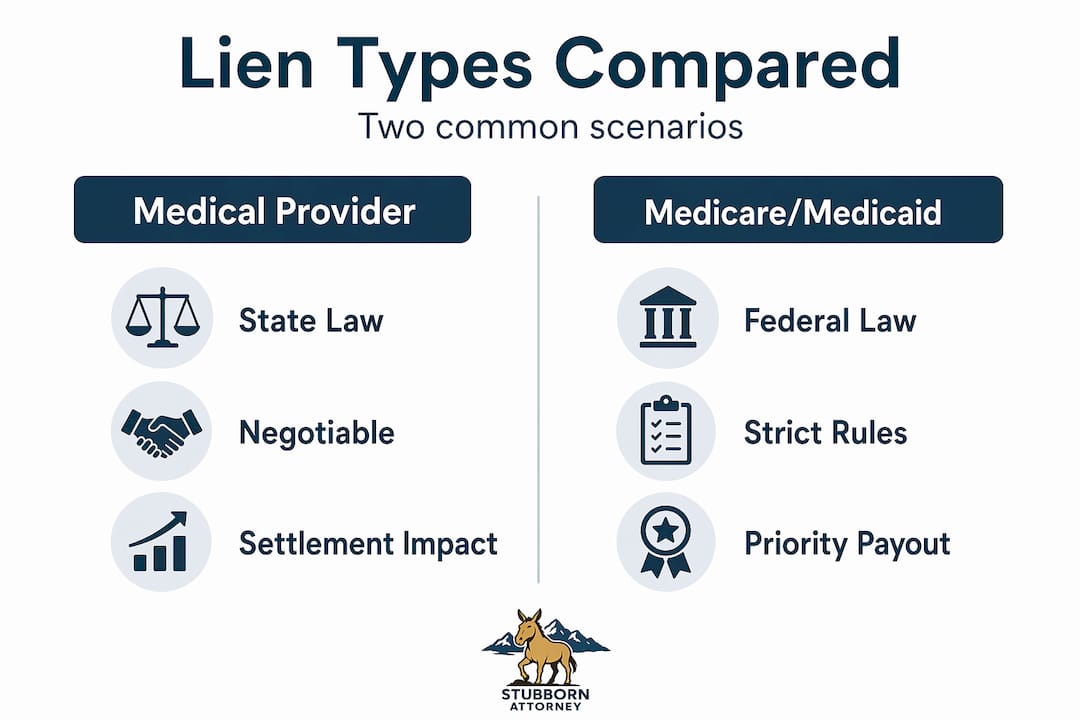

Not all liens operate the same way. Their legal authority, negotiability, and impact on your settlement vary considerably depending on the source.

| Lien Type | Authority | Negotiable? | Key Consideration |

|---|---|---|---|

| Medical provider | State statute or contract | Often yes | Must follow state filing and notice rules |

| Health insurer (subrogation) | Policy contract | Sometimes | Policy language controls recovery rights |

| Medicare | Federal law (MSP Act) | Limited | Strict federal reporting required |

| Medicaid | Federal/state law | Yes, with limits | Recent Supreme Court rulings expanded recovery |

| Workers’ comp | State statute | Varies by state | Offsets third-party recovery amounts |

| Attorney | Contract / court order | No | Secured by case proceeds, not personal assets |

Medical provider liens are the most common type you’ll encounter. A hospital or clinic files a lien against your anticipated settlement, claiming repayment for the care they provided. The rules governing these liens vary by state. Colorado, for instance, has specific requirements around notice and filing deadlines. If those procedural steps aren’t followed correctly, the lien may be invalid or unenforceable against your settlement.

Medicare liens are in a category of their own. The Medicare Secondary Payer statute is federal law, and it overrides state rules entirely. Medicare pays your injury-related bills as a “conditional payment,” meaning that payment is conditioned on being repaid when you settle. Failure to satisfy Medicare liens can lead to CMS pursuing double damages against recipients who distribute funds before the lien is satisfied. There is no room to ignore this one.

Medicaid liens have grown more complex since the Supreme Court’s 2022 ruling in Gallardo v. Marstiller, which expanded state recovery to include not just past medical expenses but future medical damages as well. This was a significant shift that caught many attorneys off guard and reshaped how Medicaid liens are calculated and negotiated.

Pro Tip: Request a complete itemized list of every conditional payment Medicare claims before your settlement is finalized. A surprising number of line items are for treatment unrelated to your accident, and those can be disputed and removed from the lien total.

How liens affect your settlement payout

Here is where understanding liens in lawsuits becomes financially critical. The settlement number your attorney negotiates is called the gross settlement. What you actually receive is the net settlement. The difference between those two numbers can be substantial, and liens are usually the biggest reason.

Resolving liens before disbursement takes time and follows a predictable sequence:

- Identify all lienholders: Your attorney sends notices to Medicare, Medicaid, health insurers, and providers early in the case. Missing a lienholder creates liability later.

- Request itemized records: Every lien claim needs documentation. Providers and government programs must supply itemized billing so your attorney can verify each charge.

- Dispute unrelated items: Proving causal relation to the accident is the hardest part. Charges for pre-existing conditions, unrelated diagnoses, or billing errors must be challenged line by line.

- Negotiate lien reductions: Most lienholders will accept less than the face value of their claim. Medicare reductions are governed by federal procurement cost formulas under 42 C.F.R. § 411.37, which reduce the lien proportionally based on attorney fees and litigation expenses. Medicaid reductions follow pro-rata allocation methods.

- Obtain lien release documentation: Before any funds are disbursed, written releases from each lienholder must be secured.

- Disburse proceeds: Only after all liens are confirmed satisfied does your attorney release your net settlement funds.

This process takes time. Long settlement timelines often result from lien verification and release requirements, not from any fault in the negotiation. Injured individuals sometimes assume their attorney is causing the delay. In reality, the attorney may be waiting on a government agency to respond to a dispute filed weeks earlier.

Multiple providers can submit separate claims, each with their own documentation requirements, creating a layered resolution process that takes weeks or months to complete.

Know this clearly: a $200,000 gross settlement after a serious injury might yield $80,000 to $120,000 in net proceeds once attorney fees, litigation costs, and lien payments are factored in. That’s not a failure. It’s the reality of how medical liens in injury settlements work, and knowing it in advance helps you plan.

Legal obligations in lien resolution

Handling liens correctly isn’t optional. There are defined legal duties that apply to both injured individuals and their attorneys, and failing to meet them creates serious risk.

The first duty is notice. For Medicare, federal law requires reporting the existence of a personal injury claim to the Centers for Medicare and Medicaid Services (CMS) well before settlement. This triggers Medicare’s obligation to identify conditional payments, and it starts the clock on your documentation process. Skipping this step doesn’t make the lien disappear. It makes your exposure worse.

The second duty is accuracy. When your attorney submits a final settlement report to Medicare or Medicaid, it must reflect the true allocation of damages. These programs are entitled to recover from the medical expense portion of your settlement. If the allocation is improper or manipulated to reduce a government lien, that creates fraud risk. Courts and CMS have seen those tactics before, and they watch for them.

For state Medicaid programs, early identification and auditing of lien claims is the most effective way to protect your net recovery. Waiting until after settlement to deal with Medicaid creates major delays and can reduce what you actually receive.

Pro Tip: Ask your attorney at the start of your case to send you a written lien inventory, listing every known or potential lienholder. Review it, ask questions, and update it as treatment continues. Clients who stay informed about their lien picture rarely get blindsided at disbursement.

Private health insurer subrogation rights depend entirely on policy language and state law. Some states have enacted anti-subrogation statutes that limit or eliminate insurer recovery rights. Colorado has its own rules in this area, and an experienced Colorado personal injury attorney will know exactly how those rules apply to your policy.

The consequences of non-compliance are serious. Distributing settlement proceeds before liens are satisfied can expose both the injured party and the attorney to personal liability. CMS has the authority to pursue double the conditional payment amount from anyone who receives settlement funds and fails to reimburse Medicare. That risk alone makes careful lien management non-negotiable.

Practical tips for managing liens in your case

You are not a passive bystander in the lien resolution process. There are concrete steps you can take from the moment your case begins that will directly affect how much money ends up in your pocket.

- Identify all potential lienholders at the start. The moment you retain an attorney, that attorney should be sending preservation letters and lien inquiry notices to every entity that paid for your care. Don’t assume this happens automatically. Ask for confirmation.

- Keep organized records of all your treatment. Every visit, every prescription, every diagnostic test tied to your injury should be documented. When lienholders submit billing that includes unrelated care, you need those records to dispute it effectively.

- Verify that every charge in a lien relates to your accident. Detailed review of non-related charges can substantially reduce what you owe. This requires requesting itemized billing from every provider and comparing it against your medical records.

- Work with an attorney who has lien negotiation experience. Lien resolution is a specialty within personal injury law. The factors affecting your settlement go well beyond the liability analysis. Attorneys who handle liens regularly know which lienholders negotiate, what reduction rates are reasonable, and how to challenge inflated claims.

- Do not accept a disbursement before all liens are cleared. It can feel frustrating to wait after a settlement is reached. But receiving funds before lien releases are obtained can trigger personal liability. Patience at this stage protects your financial outcome.

- Understand that negotiating a lien down is normal and expected. Many clients feel uncomfortable asking a hospital to accept less than full payment. The reality is that lien resolution demands collaborative negotiation between attorneys, providers, and payers. It’s not unusual to reduce a medical lien by 30 to 50 percent.

| Key Takeaway | Details |

|---|---|

| Liens attach to your settlement, not your assets | Third parties claim their share before you receive net proceeds |

| Medicare liens carry federal consequences | CMS can pursue double damages for improper disbursement |

| Medicaid recovery expanded after 2022 | Gallardo v. Marstiller allows recovery for future medical damages |

| Lien reduction is negotiable | Attorney fees and unrelated charges can reduce the lien amount owed |

| Early identification saves time and money | Proactive lien management prevents delays and maximizes net recovery |

My experience with liens and what most people get wrong

I’ve handled hundreds of personal injury cases across Colorado, and I’ll tell you something directly: liens are where most clients feel the most confused and, honestly, the most blindsided. They fought hard through their recovery, trusted the legal process, and then at the end, they’re handed a number that’s significantly smaller than what they expected. That frustration is real, and it’s legitimate.

What I’ve learned over the years is that the confusion almost always comes from the same place. People assume the settlement figure is what they’re receiving. Nobody explains early enough that the gross number and the net number are completely different conversations.

My approach now is to talk about liens on the very first call. Not as a warning or a disclaimer, but as a map. Here’s what we’re likely dealing with, here’s who will need to be paid back, and here’s where we’re going to fight to reduce those numbers. That transparency changes everything for a client’s peace of mind.

The other thing I’ve found is that improper liens get filed regularly. Hospitals include charges from pre-existing conditions. Medicare sometimes includes claims from entirely different incidents. I’ve seen Medicare conditional payment lists that included treatment from years before the accident we were litigating. Challenging those takes documentation and persistence, but it directly protects my client’s money. That’s exactly the kind of stubborn, methodical work that defines how we practice.

The clients who fare best are the ones who stay engaged. They keep their records organized, they ask questions, and they don’t panic when disbursement takes longer than expected. Managing liens properly is the difference between a good outcome and a great one.

— Ryan

How Stubbornattorney fights for your full recovery

Liens are complicated. The law around Medicare, Medicaid, and health insurer subrogation is layered, time-sensitive, and unforgiving of mistakes. At Stubbornattorney, lien resolution isn’t an afterthought. It’s a core part of how we build and close every personal injury case.

Ryan Malnar spent years as a claims adjudicator for the federal government before becoming a plaintiff’s attorney. That background means he understands how CMS evaluates Medicare liens, how adjusters think about subrogation, and exactly where the leverage exists to negotiate those numbers down. That experience directly benefits your net recovery.

Whether you’re dealing with a car accident, a slip and fall, or another type of injury, you can explore common injury case types to see how liens apply to situations like yours. If you’re ready to talk through your case and understand what liens might affect your settlement, our Colorado Springs injury team offers a free case review with no obligation. We don’t let go once we take your case. That’s not just a brand promise. That’s how we practice every single day.

FAQ

What is a lien in injury cases exactly?

A lien in an injury case is a legal claim placed on your settlement proceeds by a third party, such as a hospital, health insurer, Medicare, or Medicaid, who paid for your medical care and expects repayment from your recovery funds.

Can a medical lien reduce my entire settlement?

Liens reduce your net settlement but cannot exceed the settlement amount itself. Your attorney negotiates lien reductions to protect as much of your recovery as possible, and liens are paid from the settlement fund before you receive the remainder.

Are Medicare liens negotiable?

Medicare liens can be reduced using the federal procurement cost formula under 42 C.F.R. § 411.37, which accounts for attorney fees and litigation costs. Charges unrelated to the injury can also be disputed and removed from the lien total.

What happens if you ignore a lien on a settlement?

Ignoring a Medicare or Medicaid lien can result in CMS pursuing double the conditional payment amount from the recipient. Distributing settlement funds before all liens are resolved exposes both the client and the attorney to personal liability and enforcement action.

How long does lien resolution take after a settlement?

Lien resolution can take weeks to several months after a settlement is reached, depending on the number of lienholders, the complexity of billing disputes, and how quickly government programs respond to documentation requests.