What Is an MVA Claim? Your Complete 2026 Guide

An MVA claim is a formal request for compensation following a motor vehicle accident caused by another party’s negligence or fault. The term “MVA” stands for motor vehicle accident, and the claim itself is the legal or insurance mechanism that lets injured people recover money for medical bills, lost wages, and property damage. Understanding what an MVA claim involves is the first step toward protecting your rights after a crash. The rules governing these claims vary significantly by state and country, which means the process you follow depends entirely on where the accident happened.

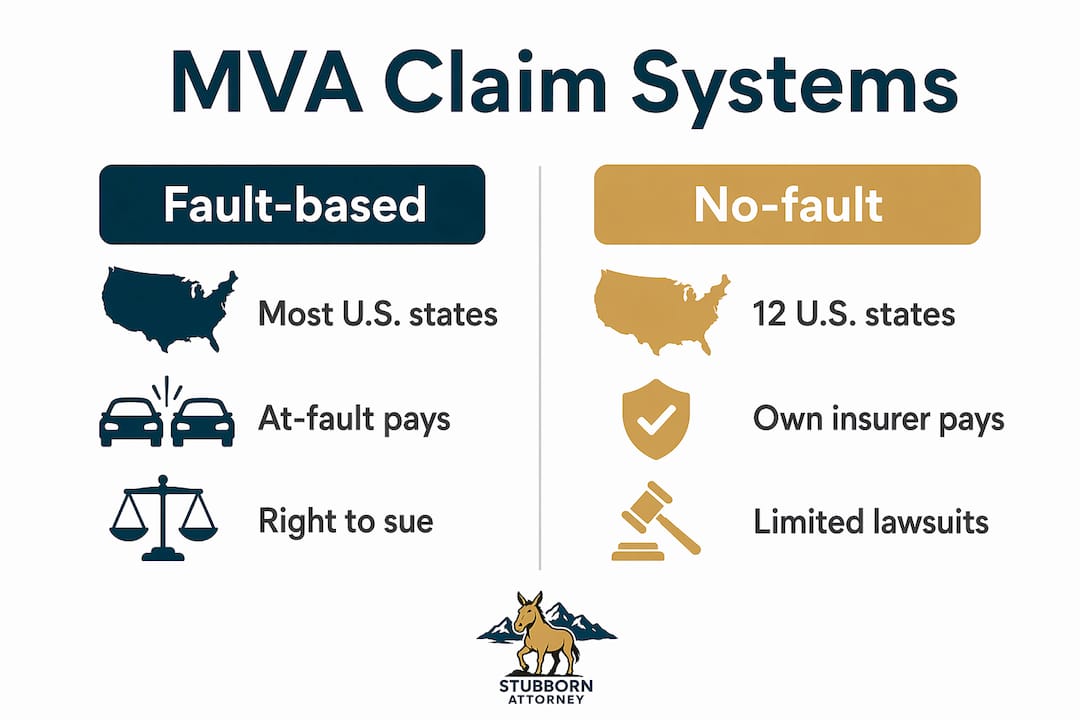

What is an MVA claim and how does it work?

An MVA claim is defined as a compensation claim filed after a vehicle collision, typically pursued through either a fault-based tort system or a no-fault insurance system. The distinction matters because it determines who pays, when you can sue, and how much you can recover.

In a fault-based tort system, the at-fault driver’s insurance pays for the victim’s damages. The injured person must prove the other driver was negligent. Most U.S. states operate this way, and Colorado is a fault state. That means if another driver caused your crash, you file a claim against their liability insurance.

No-fault systems work differently. No-fault insurance models exist in 12 U.S. states, including Florida, Michigan, New York, and New Jersey. In these states, your own insurer pays your medical bills and lost wages regardless of who caused the crash. The tradeoff is that your right to sue the at-fault driver is limited unless your injuries cross a defined severity threshold.

The governing law of your jurisdiction determines your entire claim strategy. Claimants must first identify their governing law and insurer to navigate their claim effectively. Getting this wrong at the start can cost you benefits you are legally entitled to receive.

What types of MVA claims exist across different systems?

MVA claims fall into several categories depending on the legal framework in place. The table below summarizes the key differences across major systems.

| System | Location | Who Pays | Right to Sue |

|---|---|---|---|

| Fault-based tort | Most U.S. states, Colorado | At-fault driver’s insurer | Yes, with no threshold |

| No-fault (PIP) | 12 U.S. states | Your own insurer | Only above injury threshold |

| SABS no-fault | Ontario, Canada | Your own insurer | Threshold applies |

| Motor Accidents Act | NSW, Australia | CTP insurer | 10% WPI threshold |

| MACT tribunal | India | Tribunal award | Special court process |

Ontario’s system offers a useful example of how no-fault works in practice. The Statutory Accident Benefits Schedule (SABS) provides mandatory benefits from the claimant’s own insurer regardless of fault. These benefits include medical care, rehabilitation, and income replacement. Disputes go to the Licence Appeal Tribunal (LAT) when insurers deny or reduce benefits.

New South Wales, Australia adds another layer of complexity. Claimants there pursue damages under the Motor Accident Compensation Act 1999, which imposes a 10% Whole Person Impairment threshold for pain and suffering damages. A medico-legal specialist must assess the impairment. Without meeting that threshold, non-economic damages are simply not available.

India uses Motor Accident Claims Tribunals, known as MACT. These are special courts under the Motor Vehicles Act, 1988 designed to handle injury claims without the formality of full civil litigation. Victims file a petition, hearings cover both liability and the amount owed, and the tribunal issues a compensation award.

The practical takeaway is clear. Before you file anything, confirm whether your state or country uses a fault or no-fault system. That single fact shapes every decision that follows.

What compensation can you expect from an MVA claim?

MVA claim compensation falls into three broad categories: economic damages, non-economic damages, and special damages. Each category covers a different type of loss.

Economic damages are the most straightforward. They cover measurable financial losses:

- Medical expenses, including emergency care, surgery, and ongoing treatment

- Lost wages from time missed at work during recovery

- Property damage to your vehicle and personal belongings

- Future medical costs if your injuries require long-term care

Non-economic damages cover losses that are real but harder to measure. Pain and suffering, emotional distress, and loss of enjoyment of life all fall here. In NSW, pain and suffering damages hinge on impairment assessment and cannot rest on subjective feelings alone. The claimant must plan medical documentation to align with injury severity assessments to meet the 10% impairment threshold. That is a stricter standard than most U.S. states apply.

Special damages include rehabilitation costs, income replacement benefits, and in fatal accident cases, funeral expenses and dependency claims.

Settlements in MVA claims involve negotiated agreements that compensate victims in exchange for releasing liability claims. Most cases resolve through settlement rather than a court trial. Settlement gives you certainty and speed. A court award can be larger, but it takes longer and carries more risk.

Pro Tip: Document every expense from day one. Keep receipts for prescriptions, mileage to medical appointments, and any out-of-pocket costs. Insurers and courts both respond to paper trails, not estimates.

The gap between what you are owed and what an insurer initially offers can be substantial. Knowing the full range of damages you qualify for is the foundation of any strong claim.

How to file an MVA claim: step-by-step process

Filing an MVA claim correctly from the start protects your right to full compensation. Missing a deadline or skipping a document can reduce or eliminate your recovery. Follow these steps in order.

-

Seek medical treatment immediately. Get evaluated even if you feel fine. Some injuries, like whiplash or internal bleeding, show symptoms days later. Medical records from the day of the accident anchor your claim to the event itself.

-

Report the accident to police. A police report or FIR (First Information Report in India) establishes the official record of the crash. MACT claims rely heavily on early evidence gathering, including FIR, medical records, income proof, and accident documentation to establish liability and damages.

-

Notify your insurer promptly. Most policies require notice within days of an accident. In no-fault states and provinces, your own insurer is your first point of contact. In fault states like Colorado, you will also notify the at-fault driver’s insurer.

-

Gather your documentation. The core documents for any MVA claim include:

- Police report or FIR

- Medical records and bills

- Proof of income and employment

- Photos of the accident scene and vehicle damage

- Witness contact information

- Your insurance policy details

A thorough accident evidence checklist helps you avoid missing critical items in the days after a crash.

-

Meet all filing deadlines. Strict notice periods apply in many jurisdictions, including within 6 months in NSW and India. Colorado has its own statute of limitations for personal injury claims. Missing these windows can bar your claim entirely. Review key deadlines for Colorado injury claims before you file.

-

File your claim with the correct forum. In the U.S., this usually means filing with an insurer. In India, you file a petition with the MACT. In Ontario, you file with your own insurer under SABS. Knowing the right forum prevents wasted time and procedural errors.

-

Respond to insurer requests quickly. Insurers may request recorded statements, independent medical exams, or additional documents. Delays on your end give them grounds to slow or deny your claim.

-

Negotiate or escalate. If the insurer’s offer is too low, you negotiate. If they deny the claim, you appeal or pursue a tribunal or court action. In Ontario, the LAT handles disputes. In Colorado, litigation is an option when negotiations fail.

Pro Tip: Early medical treatment is the single most powerful thing you can do for your claim. A gap between the accident and your first doctor visit gives insurers a reason to argue your injuries were not caused by the crash.

Common challenges and misconceptions in MVA claims

Most claim problems are predictable. Knowing them in advance gives you a real advantage.

-

Assuming fault always determines who pays. In no-fault systems like Ontario’s SABS, your own insurer provides benefits regardless of fault. Many accident victims never access these benefits because they wait for the other driver’s insurer to act.

-

Underestimating injury thresholds. In NSW and several no-fault U.S. states, you cannot claim non-economic damages unless your injury meets a defined severity level. Claimants often underestimate the importance of impairment assessments in claiming non-economic damages. Strategic care documentation aligned with legal thresholds is not optional. It is required.

-

Missing deadlines. Delay or failure to notify insurers or meet procedural deadlines can result in claim denial or reduced compensation. Courts may allow some discretion, but early filing is always safer.

-

Accepting the first offer. Initial settlement offers from insurers rarely reflect the full value of a claim. Insurers are trained to minimize payouts. Accepting early locks in a number that may not cover future medical costs or long-term lost income.

-

Disputes requiring tribunal intervention. Disputes with insurers over treatment plans or injury classifications often require tribunal or appeal intervention to resolve. Ontario’s LAT is one example. Knowing this path exists prevents victims from giving up when an insurer says no.

Understanding these pitfalls is not just reassuring. It is the foundation of a claim that holds up under pressure.

What I’ve learned after a decade of fighting MVA claims

After more than ten years handling personal injury cases in Colorado, and having worked as a claims adjudicator for the federal government, I have seen the same mistakes repeat themselves. The accident victims who recover the most are not the ones with the most severe injuries. They are the ones who documented everything, acted fast, and did not try to handle the insurer alone.

Insurance companies are not neutral parties. They have trained adjusters whose job is to evaluate your claim with the company’s financial interest in mind. I know this because I sat on that side of the table. The adjuster reviewing your file is not your advocate. Your attorney is.

The jurisdictional complexity in MVA claims is real. A Colorado driver involved in a crash in a no-fault state faces a completely different process than they would at home. The rules change, the forms change, and the deadlines change. Getting the framework right before you file is not a technicality. It is the difference between a full recovery and a denied claim.

One thing I tell every client: do not wait to see how you feel in a week. Get checked out the same day. Get the police report. Take photos. Call an attorney before you give a recorded statement to any insurer. These steps cost you nothing and protect everything.

— Ryan

How Stubbornattorney helps you with your MVA claim

Stubbornattorney, the brand home of Malnar Injury Law, represents only injured victims. Ryan Malnar and his team have settled hundreds of injury cases and recovered millions of dollars for people across Colorado. As a former federal claims adjudicator, Ryan knows exactly how insurers evaluate claims and where they look for reasons to pay less. That experience works directly in your favor. If you were injured in a car accident and want to understand your options, review common personal injury case examples to see how cases like yours have resolved. Then request a free case evaluation to get a clear picture of what your MVA claim may be worth.

FAQ

What does MVA stand for in a claim?

MVA stands for motor vehicle accident. An MVA claim is a formal request for compensation for injuries or property damage resulting from that accident.

How long do I have to file an MVA claim?

Deadlines vary by jurisdiction. In New South Wales and India, claimants must file within 6 months of the accident. Colorado has its own statute of limitations for personal injury claims, so acting quickly is always the safer choice.

Does fault matter in an MVA claim?

Fault matters in tort-based states like Colorado, where the at-fault driver’s insurer pays. In no-fault states and provinces like Ontario, your own insurer pays benefits regardless of who caused the crash.

What documents do I need for an MVA claim?

The core documents are a police report, medical records, proof of income, photos of the scene and vehicle damage, and your insurance policy details. Aligning these documents early dramatically improves your chances of full compensation.

Can an insurer deny my MVA claim?

Yes. Insurers can deny claims for missed deadlines, insufficient documentation, or disputed injury classifications. When that happens, dispute resolution options like Ontario’s Licence Appeal Tribunal or civil litigation in U.S. states are available paths forward.