Car Accident Damages Calculation Guide for Victims

Damages calculation is the process of quantifying every financial and non-financial loss you suffered because of a car accident, so you can support an insurance claim or legal action with real numbers. In legal practice, this process falls under the broader term “compensatory damages assessment,” which covers both economic losses you can prove with receipts and non-economic losses like pain and suffering. A solid damages calculation guide separates recoverable losses into two main categories: special damages (economic) and general damages (non-economic). Industry standards, including multiplier methods and per diem formulas, govern how courts and insurers evaluate each category. Accurate documentation and official records are the foundation of every credible claim.

What are the main categories of damages after a car accident?

Damages in law are divided into compensatory and punitive categories. Compensatory damages cover your actual losses. Punitive damages punish extreme misconduct and are rare in standard car accident claims, so this guide focuses on compensatory damages.

Economic damages (special damages)

Economic damages are quantifiable financial losses proven by invoices, wage statements, and receipts. They include:

- Medical expenses: Emergency room bills, surgery costs, physical therapy, prescription medications, and projected future treatment costs.

- Lost wages: Salary, hourly pay, commissions, bonuses, and employment benefits you could not earn while recovering.

- Property damage: Repair or replacement costs for your vehicle and any personal property destroyed in the crash.

- Out-of-pocket expenses: Transportation to medical appointments, home modifications for disability, and medical equipment like crutches or wheelchairs.

Every item on this list needs a paper trail. Without documentation, insurers treat the expense as unproven and exclude it from their offer.

Non-economic damages (general damages)

Non-economic damages cover losses that have no invoice attached. Pain and suffering, emotional distress, loss of enjoyment of life, and loss of consortium all fall into this category. These losses are real, but they require a calculation method rather than a receipt. Courts and insurers use established formulas to assign dollar values, which the next sections explain in detail.

Why the distinction matters

Compensatory damages aim to restore you to the financial position you would have occupied if the accident had never happened. This is the “but-for” principle: what your position would have been absent the accident. Keeping economic and non-economic damages clearly separated in your records makes your claim easier to verify and harder to dispute.

How to calculate economic damages step by step

Calculating financial damages starts with gathering every document that connects a dollar amount to the accident. Work through each category in sequence.

Step 1: Medical expenses

Collect every bill from every provider: hospitals, specialists, physical therapists, pharmacies, and imaging centers. Add past costs already paid to projected future costs confirmed by your treating physician. Future medical costs require a written opinion from your doctor estimating the type, frequency, and duration of ongoing treatment.

Step 2: Lost wages

Your lost wage figure must include base pay, commissions, bonuses, benefits, and retirement contributions. Ignoring bonuses and benefits commonly undervalues claims by thousands of dollars. Gather pay stubs covering the 12 months before the accident, your employer’s written confirmation of missed workdays, and any documentation of lost promotions or career opportunities.

Step 3: Property damage

Get at least one written repair estimate from a licensed body shop. If the insurer declares the vehicle a total loss, the standard is fair market value at the time of the accident, not the price you originally paid. Keep receipts for any personal property destroyed in the crash, such as a laptop or child safety seat.

Step 4: Out-of-pocket expenses

Track every cost the accident created that is not already captured above. Rideshare receipts to medical appointments, parking fees at the hospital, and the cost of hiring help for household tasks you can no longer perform all count. These costs are easy to overlook and easy to prove with receipts.

Economic damages reference table

| Damage category | Key documents needed | Basic formula |

|---|---|---|

| Medical expenses | Bills from all providers, physician future-cost letter | Past costs + projected future costs |

| Lost wages | Pay stubs, employer letter, tax returns | Daily rate × missed workdays + lost benefits |

| Property damage | Repair estimates, total-loss valuation | Repair cost or fair market value |

| Out-of-pocket costs | Receipts, mileage log | Sum of all verified expenses |

Pro Tip: Request itemized bills from every health provider, not summary statements. Itemized medical statements prevent insurers from dismissing charges as “unnecessary,” because each line item shows exactly what treatment was provided and why.

Effective methods to calculate non-economic damages

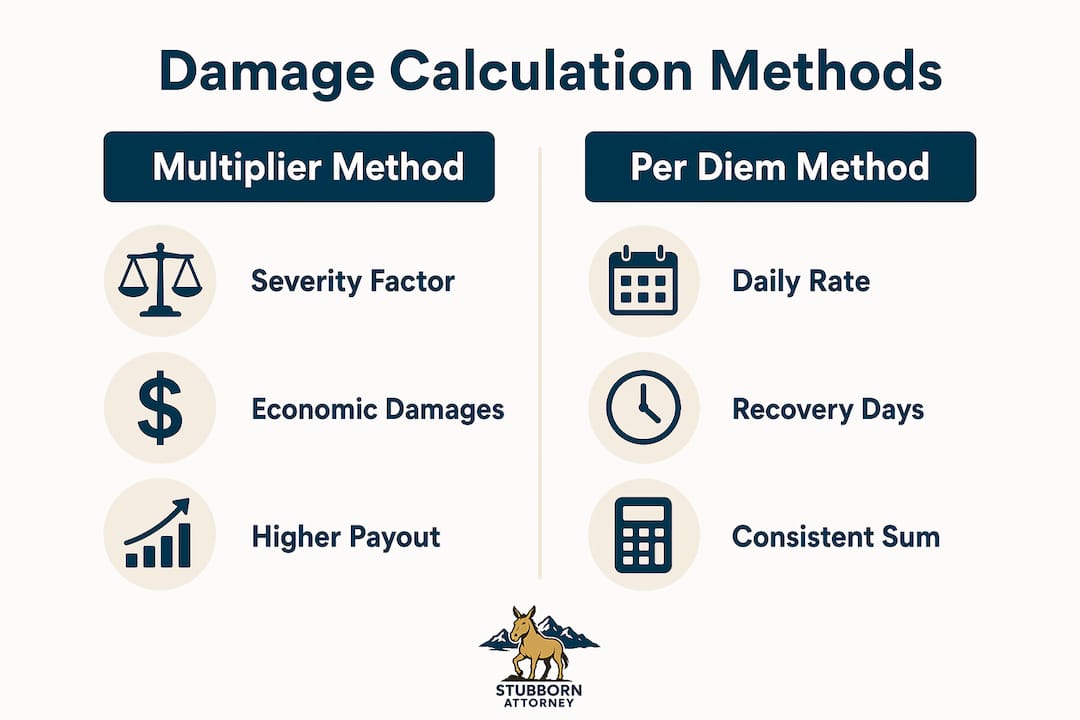

Non-economic damages have no receipt, so calculating them requires a recognized formula. Two methods dominate personal injury practice: the multiplier method and the per diem method.

The multiplier method

The multiplier method multiplies your total economic damages by a number that reflects injury severity. The multiplier typically ranges from 1.5 to 5, with higher numbers reserved for severe, permanent injuries. A minor soft-tissue injury might use a 1.5 multiplier. A spinal injury requiring surgery and long-term care might justify a 4 or 5.

Example: $80,000 in economic damages multiplied by a factor of 3 produces $240,000 in non-economic damages. Your total compensatory claim would be $320,000.

Factors that push the multiplier higher include permanent disability, disfigurement, long recovery timelines, and strong medical documentation of suffering.

The per diem method

The per diem method assigns a daily dollar value to your pain and suffering, then multiplies it by the number of days you suffered. The daily value is often linked to your daily earnings, which gives the figure a defensible basis.

Example: A daily rate of $250 multiplied by 400 days of documented recovery equals $100,000 in non-economic damages.

Comparing the two methods

| Method | Best used when | Potential weakness |

|---|---|---|

| Multiplier | Economic damages are well-documented and substantial | High multipliers require strong medical support |

| Per diem | Recovery period is clearly defined and documented | Daily rate can be challenged if not tied to earnings |

Neither method produces a guaranteed outcome. Insurers apply their own formulas, and courts weigh the evidence independently. The method you use should match the facts of your case.

Pro Tip: Document your pain and limitations in a daily journal from the day of the accident. Judges and adjusters find personal journals credible because they show a real-time record of suffering, not a reconstructed account.

Common challenges in gathering evidence and verifying damage calculations

Evidence problems are the most common reason strong claims receive low offers. Knowing where documentation fails helps you avoid the same mistakes.

- Summary bills instead of itemized bills: A one-page summary from a hospital gives insurers grounds to question every charge. Request a line-by-line itemized statement from each provider.

- Incomplete wage records: Many claimants submit only base salary records. Lost wages calculations must include commissions, bonuses, benefits, and retirement contributions to reach an accurate total.

- Gaps in the medical timeline: A gap between the accident date and your first medical visit gives insurers a reason to argue the injury was not caused by the crash. Seek medical attention immediately after any accident, even if symptoms seem minor.

- Weak causation documentation: Causation must be explicitly demonstrated through a documented chronology linking the accident to each financial loss. Your medical records, accident report, and billing records must tell a consistent, connected story.

- Forgotten out-of-pocket costs: Mileage, parking, home care, and medical equipment costs are easy to forget and easy to prove. Keep a running expense log with receipts from day one.

- Unaddressed mitigation obligations: Claimants must take reasonable steps to minimize their losses. Refusing recommended treatment or ignoring medical advice gives the opposing party grounds to reduce your calculable damages.

Cross-check your totals against your original documents before submitting anything. A single math error or missing receipt can create doubt about the entire claim.

Pro Tip: Use a spreadsheet to log every expense by date, category, and supporting document. A well-organized expense log signals to adjusters and attorneys that your claim is thorough and credible.

How to validate and finalize your damages calculation

Reviewing your totals before submission catches errors that could cost you thousands. Follow these steps to confirm your numbers are accurate and defensible.

- Reconcile economic and non-economic totals separately. Add up every economic category independently, then apply your chosen non-economic method. Never mix the two until you have confirmed each subtotal.

- Have an attorney or damages expert review your assumptions. Damages models must be transparent and grounded in contemporaneous records to survive scrutiny. A professional review catches errors you cannot see yourself.

- Discount future losses to present value. Discounting future damages to present value using an appropriate discount rate is required when losses extend over years. Small changes in the discount rate significantly affect the final number, so use a qualified financial expert for this step.

- Prepare a clear written summary. Organize your damages into a one-page summary showing each category, the total, and the supporting documents. Insurers and courts respond better to organized presentations than to stacks of unsorted bills.

- Confirm your injury case value with a legal professional. Colorado personal injury law includes specific rules about damage caps and comparative fault that affect your final recoverable amount.

- Avoid last-minute additions. Adding new expenses after you submit a demand letter weakens your credibility. Compile a complete record before you make any offer or demand.

Why I treat damages calculation as a discipline, not an estimate

After more than a decade handling personal injury cases in Colorado, and years before that as a federal claims adjudicator, I have seen one pattern repeat itself: the claimants who receive the lowest offers are almost always the ones who treated their damages calculation as an afterthought.

Insurance adjusters are trained to find gaps. A missing bonus in a lost wage calculation, a summary bill instead of an itemized one, a gap in the medical timeline. Each gap becomes a reason to reduce the offer. I have watched clients leave significant money on the table not because their injuries were minor, but because their documentation was incomplete.

The number that surprises most people is how much non-economic damages contribute to a fair settlement. Claimants who focus only on their medical bills routinely undervalue their claims. Pain, suffering, and lost quality of life are real losses. The multiplier method and per diem method exist precisely because courts and insurers recognize that. But those methods only work when the underlying economic damages are fully documented and the medical record clearly supports the severity of the injury.

My advice is to treat your damages calculation the way you would treat a tax return. Every number needs a source document. Every category needs to be complete. And the whole thing needs to be reviewed by someone who knows what opposing counsel or an adjuster will look for. The factors that affect your settlement go beyond the math, but the math has to be right first.

— Ryan

How Stubbornattorney can help you calculate and recover your full damages

Stubbornattorney, the Colorado personal injury practice of Ryan Malnar, has settled hundreds of injury cases and recovered millions of dollars for clients across the state. Ryan’s background as a former federal claims adjudicator means he knows exactly how insurance companies evaluate your numbers, and where they look for reasons to pay less. The team at Stubbornattorney reviews your economic and non-economic damages, identifies gaps in documentation, and builds a calculation that holds up under scrutiny. If you were injured in a car accident, a free case evaluation gives you a clear picture of what your claim is worth before you accept any offer. You can also review common personal injury case examples to see how damages play out in real claims similar to yours.

FAQ

What is a damages calculation in a car accident claim?

A damages calculation is the process of quantifying every financial and non-financial loss caused by a car accident to support an insurance claim or lawsuit. It covers economic losses like medical bills and lost wages, and non-economic losses like pain and suffering.

How do I calculate pain and suffering damages?

The two standard methods are the multiplier method and the per diem method. The multiplier method multiplies total economic damages by a factor of 1.5 to 5 based on injury severity; the per diem method assigns a daily dollar value and multiplies it by the number of days you suffered.

What documents do I need to calculate economic damages?

You need itemized medical bills from every provider, pay stubs and an employer letter confirming missed work, repair estimates or a total-loss valuation for your vehicle, and receipts for all out-of-pocket expenses. Complete wage records must include bonuses, commissions, and benefits, not just base salary.

What is the “but-for” principle in damages calculation?

The but-for principle means your damages equal the difference between your actual financial position and the position you would have been in if the accident had never happened. It is the foundational standard courts use to measure compensatory damages in personal injury cases.

Can I lose damages if I do not follow medical advice?

Yes. Claimants have a legal duty to mitigate their losses by taking reasonable steps to recover. Failing to follow prescribed treatment gives the opposing party grounds to reduce your calculable damages, because the additional harm is considered self-inflicted rather than caused by the accident.