What Is Property Damage Liability in Car Insurance?

Property damage liability insurance is defined as the coverage that pays to repair or replace someone else’s property when you cause damage in a car accident. Known formally as PDL coverage, it is a mandatory component of auto insurance in nearly every U.S. state as of 2026. State minimums range from $5,000 to $25,000, but experts recommend carrying at least $100,000 in coverage. PDL covers only third-party property. It does not pay for damage to your own vehicle or belongings. Understanding what is property damage liability, how it works, and where its limits fall can be the difference between financial security and a lawsuit that follows you for years.

What is property damage liability and what does it cover?

Property damage liability is the portion of your auto insurance policy that pays for damage you cause to another person’s property. The coverage applies when you are found at fault in an accident. It does not matter whether the damaged property is a car, a fence, a storefront, or a utility pole. If you caused the damage, your PDL coverage pays the bill up to your policy limit.

PDL coverage is strictly third-party protection. That distinction is critical. Your own vehicle is not covered under this portion of your policy. To protect your own car, you need separate first-party coverages like collision or comprehensive insurance.

The types of property covered under a standard PDL policy go well beyond other vehicles. Common examples include:

- Other drivers’ cars and trucks

- Fences, walls, and landscaping

- Residential and commercial buildings

- Streetlights, guardrails, and utility poles

- Equipment, signage, and other physical structures

Property damage liability is also a key component of commercial general liability policies, not just personal auto insurance. A business owner whose employee causes an accident in a company vehicle relies on the same PDL framework for third-party property protection.

Pro Tip: Check your declarations page right now. The PDL limit is listed as a single dollar amount, such as $25,000 or $100,000. That number is the maximum your insurer will pay per accident, not per damaged item.

How does property damage liability insurance work after an accident?

A PDL claim begins the moment you report an at-fault accident to your insurer. The insurer then investigates to confirm fault, assess the damage, and determine how much it owes the third party. This process typically involves reviewing police reports, photos, witness statements, and repair estimates.

Once fault is established, your insurer pays the third party directly up to your policy limit. You generally do not pay a deductible on a PDL claim. Property damage liability policies rarely include deductibles because the coverage compensates third parties rather than the insured’s own property. That is a meaningful difference from collision or comprehensive coverage, which almost always carry a deductible.

The financial risk appears when damages exceed your policy limit. If the other driver’s car costs $40,000 to replace and your PDL limit is $25,000, your insurer pays $25,000. The remaining $15,000 becomes your personal responsibility. Costs exceeding policy limits can lead to court judgments and seizure of personal assets. That is not a hypothetical. It happens regularly in accidents involving newer vehicles or commercial property.

Your liability coverage also pays for your legal defense if the other party sues you. Liability insurance covers legal defense costs including attorney fees and court expenses, even for claims that turn out to be groundless. That protection alone justifies carrying more than the state minimum.

To understand how a property damage claim unfolds step by step after a collision, the process involves more moving parts than most drivers expect.

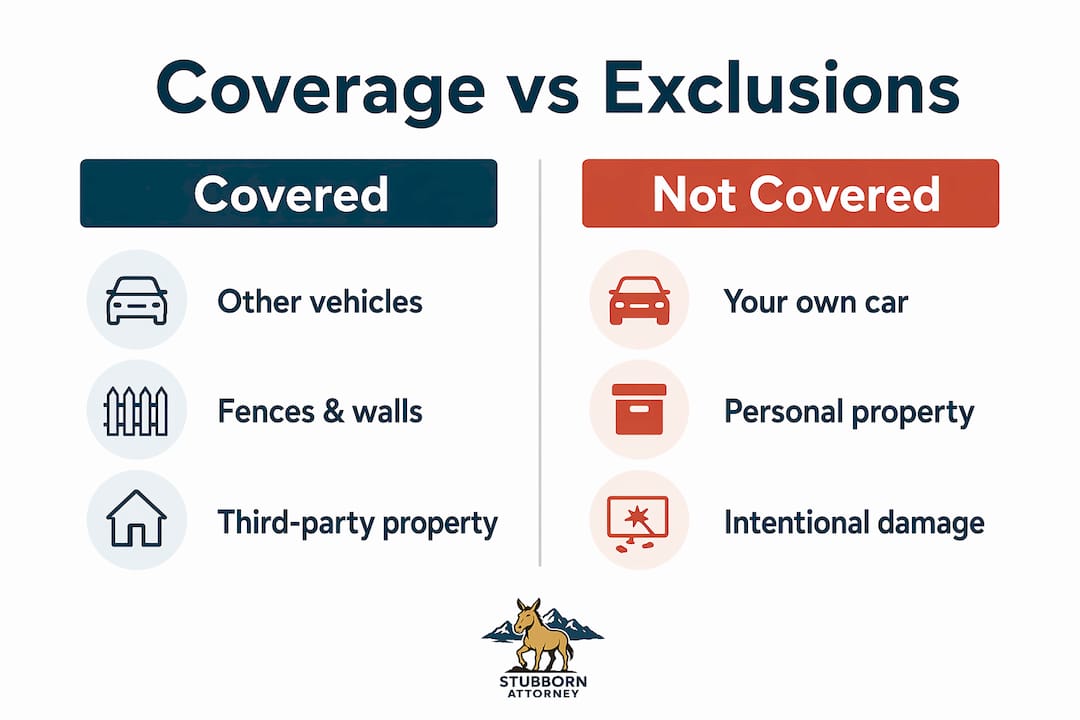

What types of property damage are covered and what is excluded?

The scope of PDL coverage is broad when it comes to third-party property, but it has a firm boundary. Anything belonging to you is excluded.

| Covered by PDL | Not Covered by PDL |

|---|---|

| Other driver’s vehicle | Your own vehicle |

| Fences and walls | Your personal belongings in the car |

| Buildings and storefronts | Your home or property |

| Streetlights and utility poles | Injuries to yourself |

| Equipment and signage | Medical bills for any party |

The most common misconception drivers carry is that liability covers their own damages. Many drivers mistakenly believe liability covers their own vehicle, which leads to inadequate first-party coverage and unexpected out-of-pocket repair costs. If you total your own car in an at-fault accident and you have no collision coverage, you pay for your own repairs entirely.

Collision insurance covers damage to your vehicle regardless of fault. Comprehensive insurance covers non-collision events like theft, hail, or flooding. Both are optional under most state laws, though lenders typically require them if you are financing or leasing a vehicle.

Pro Tip: If you drive a vehicle worth more than $15,000, carrying collision coverage alongside your PDL policy is not optional in any practical sense. State minimum PDL limits will not touch your own repair bill.

State minimum PDL limits vary widely. Florida requires just $10,000. California requires $5,000 for property damage. Those figures reflect the cost of vehicles from decades past. State minimums as low as $5,000 to $25,000 are often insufficient for modern vehicle damage costs. A single rear-end collision involving a newer SUV or truck can easily exceed those limits.

Understanding the full range of car accident claim types helps clarify where PDL fits within the broader legal and insurance picture after a collision.

Why choosing the right coverage limit is critical for financial protection

The gap between state minimum PDL limits and real-world accident costs is wide enough to bankrupt a household. State minimums frequently fail to cover the total loss of newer vehicles, exposing drivers to substantial personal liability for the excess. A $25,000 PDL limit sounds reasonable until you hit a $60,000 pickup truck.

Experts consistently recommend at least $100,000 in property damage liability coverage. The cost difference is smaller than most drivers assume. Increasing from minimum limits to $100,000 in PDL coverage often costs just $5 to $15 more per month. That is a modest premium increase compared to the potential exposure of a five-figure judgment against you.

The financial consequences of underinsuring break down into three categories:

- Out-of-pocket repair costs. You pay the difference between the actual damage and your policy limit directly to the other party or through a court order.

- Civil lawsuits. The other party can sue you personally for the excess amount. A judgment against you can attach to your wages, bank accounts, and property.

- Asset seizure. Courts can order the seizure of personal assets to satisfy a judgment. This includes savings accounts, real estate equity, and future earnings.

Liability coverage also functions as a legal defense shield, covering attorney fees and court costs regardless of whether the claim against you has merit. Without it, defending even a frivolous lawsuit costs thousands of dollars before you ever reach a verdict.

Umbrella policies offer an additional layer of protection above your standard auto insurance limits. Umbrella insurance provides extra liability coverage beyond what your primary auto policy pays. For drivers with significant assets, an umbrella policy is a practical way to extend PDL protection without restructuring your entire auto policy.

Reviewing your bodily injury liability coverage in Colorado alongside your PDL limits gives you a complete picture of your total liability exposure after an accident.

How does property damage liability fit with other auto insurance coverages?

PDL is one piece of a larger coverage structure. Understanding how it interacts with other policies prevents gaps that leave you exposed after an accident.

| Coverage Type | What It Pays For | Covers Your Vehicle? | Deductible? |

|---|---|---|---|

| Property damage liability | Others’ property damage | No | No |

| Collision | Your vehicle after a crash | Yes | Yes |

| Comprehensive | Your vehicle, non-collision events | Yes | Yes |

| Umbrella | Excess liability above all limits | No | No |

The most important distinction is the third-party versus first-party divide. PDL pays others. Collision and comprehensive pay you. These coverages do not overlap, and they do not substitute for each other. A driver who carries only state minimum PDL and no collision coverage is fully exposed to their own vehicle repair costs in any at-fault accident.

Confusion about liability versus collision coverage creates insurance gaps that jeopardize financial protection after accidents. This confusion is one of the most common and costly mistakes drivers make. They assume their insurance “covers the accident” without realizing that phrase means very different things depending on whose property was damaged.

Umbrella policies sit above all primary coverages. They activate only after your auto policy limits are exhausted. A driver with $100,000 in PDL and a $1 million umbrella policy has $1.1 million in total property damage liability protection. That level of coverage is appropriate for anyone with significant assets or a high risk of being involved in a serious accident.

The practical takeaway is straightforward. Build your coverage from the ground up: start with PDL at $100,000 or higher, add collision and comprehensive for your own vehicle, and consider an umbrella policy if your assets exceed your auto policy limits. Knowing how to claim and win after an auto accident also depends on understanding which coverage applies to which part of the loss.

What I’ve learned about PDL coverage after years of handling accident claims

Most drivers treat property damage liability as a checkbox. They buy the minimum, pay the premium, and assume they are covered. After more than a decade handling personal injury and accident claims in Colorado, I can tell you that assumption causes real financial harm.

The cases that concern me most are not the catastrophic accidents. They are the ordinary ones. A driver runs a red light and hits a newer pickup truck. The truck is a total loss at $55,000. The driver carries $25,000 in PDL. The insurer pays $25,000. The driver now owes $30,000 personally, and the truck owner’s attorney files suit within 60 days. That scenario plays out constantly.

The $5 to $15 per month difference between minimum and adequate PDL limits is the most undervalued financial decision most drivers make. I have never had a client tell me they wished they had carried less coverage. I have had many tell me they wished they had carried more.

My practical advice is direct. Call your insurer today and ask what it costs to raise your PDL limit to $100,000. If you have assets worth protecting, ask about umbrella coverage. And if you are ever in an accident where the other driver’s insurer is pushing back on a claim, get legal advice before you sign anything. Insurance companies evaluate claims to minimize payouts. You deserve someone in your corner who evaluates them to maximize your recovery.

— Ryan

When a property damage dispute becomes a legal matter

Property damage liability questions become legal problems faster than most people expect. When an insurer denies a claim, disputes fault, or offers a settlement that does not cover the actual damage, you need more than a policy number. You need representation.

Stubbornattorney has settled hundreds of injury and accident cases across Colorado, recovering millions of dollars for people dealing with exactly these situations. Ryan Malnar spent years as a federal claims adjudicator before becoming a personal injury attorney. He knows how insurers evaluate claims because he used to do it. That background means Stubbornattorney approaches every personal injury case with the same knowledge the other side uses. If you are facing a property damage dispute or need help understanding your coverage after an accident, a free case review costs you nothing and could change everything.

FAQ

What is property damage liability in simple terms?

Property damage liability is the part of your auto insurance that pays to repair or replace someone else’s property when you cause an accident. It covers vehicles, fences, buildings, and other third-party property up to your policy limit.

Does property damage liability cover my own car?

No. PDL covers only damage you cause to others’ property. Damage to your own vehicle requires collision coverage, which is a separate first-party policy with its own deductible.

What happens if my PDL limit is too low?

If the damage you cause exceeds your PDL limit, you are personally responsible for the difference. The other party can sue you, and a court can order wage garnishment or asset seizure to collect the excess amount.

Does property damage liability have a deductible?

Property damage liability generally does not have a deductible because it compensates third parties rather than the insured. Collision and comprehensive coverages, which cover your own vehicle, typically do carry a deductible.

How much property damage liability coverage should I carry?

Experts recommend at least $100,000 in PDL coverage. The cost increase from state minimum limits to $100,000 is often just $5 to $15 per month, making it one of the most cost-effective financial protections available to drivers.