Understanding financial compensation after a crash in Colorado

TL;DR:

- Insurance companies aim to pay as little as possible, often leaving victims undercompensated.

- Proper documentation of all damages and quick action can significantly improve compensation outcomes.

- Consulting a personal injury attorney increases the likelihood of receiving full and fair settlement amounts.

Most people assume their insurance policy will take care of everything after a car accident. That assumption can cost you thousands of dollars. The reality is that insurance companies are businesses, and their goal is to pay out as little as possible on every claim. Colorado accident victims often discover too late that their coverage gaps are wide, their injuries are more expensive than expected, and the compensation they accepted was far below what they actually deserved. This guide breaks down exactly what financial compensation means after a crash, how it gets calculated, what obstacles stand in your way, and the specific steps you can take right now to protect your recovery.

Table of Contents

- What financial compensation means after a Colorado crash

- How financial compensation is calculated after a car accident

- Common challenges in getting fair compensation

- Steps to take after a crash to maximize your compensation

- Why most Colorado crash victims settle for less than they deserve

- Find expert support for your Colorado accident claim

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your rights | Insurance rarely covers all losses, so understanding compensation is essential. |

| Documentation matters | Careful recordkeeping strengthens your claim and can significantly improve your outcome. |

| Legal advice is key | Consulting an experienced attorney improves your chances of a fair settlement. |

| Act quickly | Strict deadlines mean prompt action protects your right to financial recovery. |

What financial compensation means after a Colorado crash

When attorneys and courts talk about financial compensation after a car accident, they mean the total amount of money you are legally entitled to receive for every loss the crash caused. That includes costs you can add up on a spreadsheet and losses that are harder to put a dollar figure on. Both categories matter, and both are recoverable under Colorado law.

The legal system divides compensation into two main buckets: economic damages and non-economic damages.

Economic damages cover your measurable, out-of-pocket losses. These are the expenses you can document with receipts, bills, and pay stubs. Examples include:

- Emergency room visits and hospital stays

- Surgery, physical therapy, and ongoing medical treatment

- Prescription medications and medical equipment

- Lost wages from time missed at work

- Future lost earning capacity if your injury affects your ability to work long-term

- Vehicle repair or replacement costs

- Transportation to medical appointments

Non-economic damages cover the real but harder-to-measure harm the crash caused to your life. Colorado law recognizes these losses as legitimate, and they often represent the largest portion of a settlement. Examples include:

- Physical pain and suffering

- Emotional distress and anxiety

- Loss of enjoyment of life

- Damage to personal relationships (sometimes called loss of consortium)

- Permanent disfigurement or disability

Colorado follows an at-fault system for car accidents, meaning the driver who caused the crash is responsible for covering the damages. The injury settlement examples from real Colorado cases show how widely compensation amounts can vary depending on injury severity, fault determination, and how well the victim documented their losses.

One thing that surprises many accident victims is how quickly costs add up. A single emergency room visit in Colorado can run $3,000 to $10,000 before any follow-up care. Add physical therapy, lost work time, and vehicle damage, and you are looking at a number that most insurance minimum limits simply cannot cover.

| Type of damage | Examples | Typically documented by |

|---|---|---|

| Economic | Medical bills, lost wages, property damage | Receipts, pay stubs, repair estimates |

| Non-economic | Pain, emotional distress, loss of enjoyment | Medical records, personal journals, testimony |

Pro Tip: Start a dedicated folder, physical or digital, the day of your accident. Save every receipt, every bill, every email from your employer about missed work, and every note your doctor gives you. This habit alone significantly increases the value of your claim.

How financial compensation is calculated after a car accident

Knowing what types of compensation exist is one thing. Understanding how the actual dollar amount gets determined is where most accident victims feel lost. The calculation is not random, but it is also not a simple formula. Several factors pull the number up or down.

Here is a straightforward breakdown of how damages are typically estimated:

- Add up all economic losses. Start with every documented expense: medical bills paid and expected, lost income to date, future medical costs estimated by your doctors, and property damage.

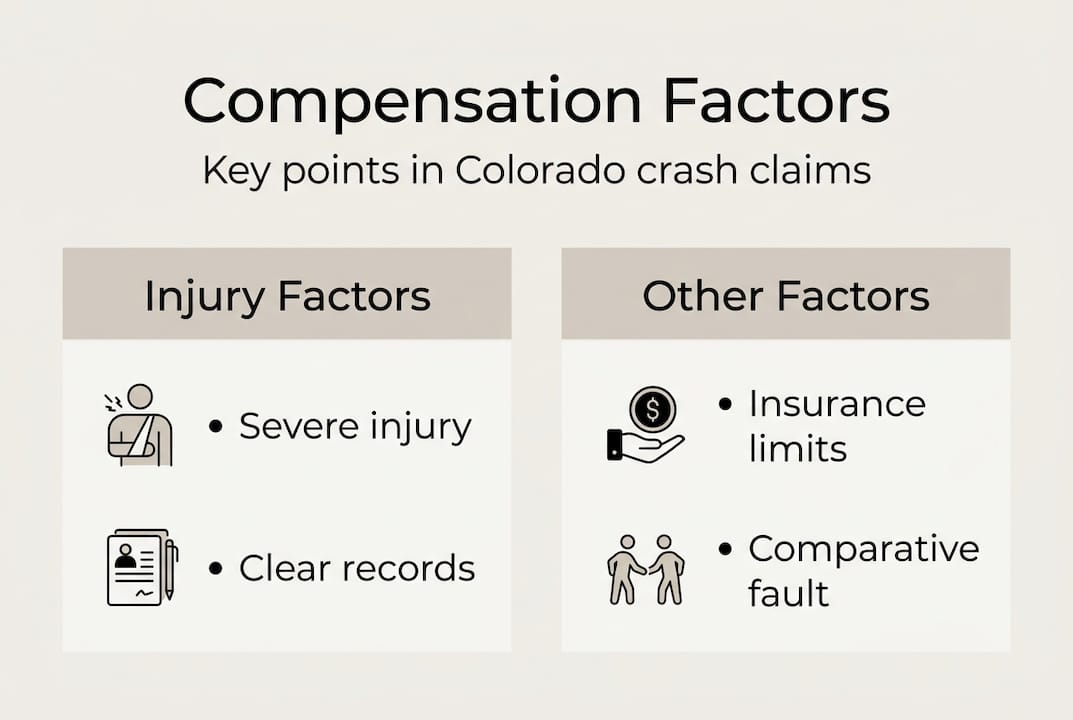

- Estimate non-economic damages. Attorneys and insurance adjusters often use a multiplier method, taking your total economic damages and multiplying by a number between 1.5 and 5, depending on injury severity. A serious, permanent injury might use a higher multiplier.

- Factor in insurance policy limits. Even if your damages are $300,000, the at-fault driver’s policy may only cover $25,000. Knowing the limits of every applicable policy matters early in the process.

- Apply Colorado’s comparative fault rule. If you were partly responsible for the crash, your compensation is reduced by your percentage of fault. If you are found 20% at fault, you receive 20% less.

- Compare the offer to actual losses. Insurance companies rarely open with a fair number. Their first offer is a starting point, not a final answer.

“The gap between what an insurance company first offers and what a victim actually deserves is often staggering. Documentation and persistence close that gap.”

The lawsuit process in Colorado can take months or even years, and the strength of your documentation at every stage directly shapes your outcome. Cases with thorough medical records, clear evidence of lost income, and credible witness statements consistently result in higher settlements.

| Factor | Effect on compensation |

|---|---|

| Severe or permanent injury | Increases value significantly |

| Strong medical documentation | Supports higher economic and non-economic claims |

| Partial fault assigned to victim | Reduces compensation proportionally |

| Low at-fault driver policy limits | May cap recovery without underinsured motorist coverage |

| Delay in seeking medical treatment | Gives insurers grounds to dispute injury severity |

One often-overlooked factor is underinsured motorist (UIM) coverage on your own policy. If the at-fault driver’s insurance is not enough, your own UIM coverage can fill the gap. Many Colorado drivers carry it without realizing how valuable it is after a serious crash.

Common challenges in getting fair compensation

Understanding the calculation is helpful, but the path to fair compensation is rarely smooth. Insurance companies have trained professionals whose job is to minimize what they pay you. Knowing their tactics puts you in a better position to push back.

Common insurance adjuster tactics include:

- Calling you within days of the accident to get a recorded statement while you are still in shock

- Offering a quick cash settlement before you know the full extent of your injuries

- Arguing that your injuries were pre-existing or not caused by the crash

- Delaying the claim process, hoping you will accept less out of frustration

- Disputing the necessity of certain medical treatments

A car accident legal checklist can help you recognize these tactics before they cost you money. Victims who go in without preparation are far more likely to accept offers that do not reflect their true losses.

Mistakes that can seriously hurt your case:

- Giving a recorded statement to the other driver’s insurer without legal advice

- Posting about the accident or your injuries on social media

- Skipping or delaying medical appointments after the crash

- Accepting a settlement before finishing medical treatment

- Failing to report the accident to your own insurance company

The lack of documentation is one of the most common and most damaging pitfalls. If you cannot prove a loss happened, it becomes very difficult to recover money for it. Medical evidence is especially critical. Gaps in treatment give adjusters an opening to argue your injuries were not serious or were caused by something else.

Witness statements also carry real weight. If anyone saw the crash, their contact information is worth collecting at the scene. A neutral third-party account can counter an at-fault driver’s version of events and strengthen your position significantly.

Statistic callout: Studies show that accident victims represented by an attorney receive settlements that are, on average, three to four times higher than those who negotiate alone.

Pro Tip: Never accept any settlement offer, even a small one, without first speaking to a personal injury attorney. Once you sign a release, you typically cannot go back for more money, even if your medical costs turn out to be far higher than expected.

Steps to take after a crash to maximize your compensation

Knowing the pitfalls is only useful if you also know what to do instead. The actions you take in the hours and days after a crash have a direct impact on the strength of your claim.

“The decisions you make in the first 48 hours after a crash often determine the ceiling on your compensation.”

Immediate steps at the scene:

- Call 911. Get law enforcement and, if needed, emergency medical services to the scene. A police report is one of the most important documents in your case.

- Seek medical attention right away. Even if you feel fine, some injuries like whiplash and internal bleeding do not show symptoms immediately. See a doctor the same day or the next morning.

- Document the scene. Take photos and video of vehicle damage, road conditions, traffic signals, skid marks, and any visible injuries.

- Collect information. Get the other driver’s name, license number, insurance company, and policy number. Note the names and contact details of any witnesses.

- Do not admit fault. Even saying “I’m sorry” can be used against you later.

In the days that follow:

- Report the accident to your own insurance company, but keep your statement factual and brief.

- Follow all medical advice. Attend every appointment and follow through on prescribed treatment.

- Keep a personal injury journal. Write down how your injuries affect your daily life, your sleep, your ability to work, and your emotional state.

- Avoid social media. Insurance adjusters routinely monitor claimants’ accounts.

- Contact a personal injury attorney. The reasons to pursue a claim are compelling, and an attorney can identify compensation categories you might not know to ask for.

Essential documents to keep for your case:

- Police report and accident number

- All medical records and bills

- Photos and videos from the scene

- Witness contact information

- Correspondence with insurance companies

- Pay stubs showing lost income

- Receipts for all out-of-pocket expenses related to the crash

Every item on that list is a building block for your claim. The more complete your records, the harder it is for an insurance company to dispute what you are owed.

Why most Colorado crash victims settle for less than they deserve

After years of working injury cases and a background as a former federal claims adjudicator, I have seen a pattern repeat itself more times than I can count. Victims who deserve substantial compensation walk away with a fraction of it, not because the law failed them, but because they made a few avoidable decisions early on.

The most common reason is trust. People assume the insurance company is there to help them. It is not. The adjuster assigned to your case works for the insurer, not for you. Their performance is measured, in part, by how much they save the company on each claim.

The second reason is urgency. After a crash, life is stressful. Bills pile up. You want it to be over. That emotional pressure is exactly what early settlement offers are designed to exploit. Accepting fast money feels like relief, but it almost always means leaving far more on the table.

The third reason is fear. Many people worry that pursuing a claim will be confrontational, expensive, or time-consuming. In reality, most personal injury cases resolve without going to trial, and most attorneys work on contingency, meaning you pay nothing unless you win.

Looking at real settlement outcomes from Colorado cases makes the stakes clear. The difference between a victim who documented everything, waited for full medical clarity, and worked with an attorney versus one who accepted the first offer can be tens of thousands of dollars. That is not a small gap. It is the difference between financial recovery and financial hardship.

Find expert support for your Colorado accident claim

If you have been hurt in a crash in Colorado, you do not have to figure this out alone. At Malnar Injury Law, our Colorado injury lawyers have spent years doing exactly one thing: fighting for injured victims. We have settled hundreds of cases and recovered millions of dollars for people who were told by insurance companies that their claim was worth far less.

Ryan Malnar brings something most attorneys cannot offer: real experience as a former federal claims adjudicator. He knows how insurers think, how they evaluate claims, and where they look for weaknesses. That inside knowledge shapes every case we take.

We offer free consultations with no obligation. Whether you are just starting to think about pursuing your injury case or you have already received an offer that does not feel right, we can help you understand your options. Take the first step and protect your rights after a crash by reaching out today.

Frequently asked questions

How long do I have to file a compensation claim after a car accident in Colorado?

In Colorado, you generally have three years from the date of the accident to file a personal injury claim, as outlined by the state’s statute of limitations. Missing this deadline almost always means losing your right to recover any compensation.

What should I do if the insurance company offers a quick settlement?

Be cautious. Quick settlements are typically far below what your case is actually worth, and the risks of early offers are well-documented. Always consult an attorney before signing anything.

Can I claim compensation if I was partially at fault for the accident?

Yes. Colorado uses a modified comparative fault rule, meaning you can still recover damages as long as you are less than 50% responsible. Real Colorado case outcomes show that partial fault does not automatically disqualify your claim.

Are non-economic damages like pain and suffering included in compensation?

Yes. Colorado law allows injured parties to claim non-economic damages including pain, suffering, and emotional distress. These non-economic damages often represent a significant portion of the total compensation in serious injury cases.